Skip to content

Skip to content

In 2014, on my first day at Intel, my manager welcomed me to the team and told me that I just joined the best team in the world. At the time, I joined the team that was developing the 10nm chip node, which was the next state-of-the-art chip back then.

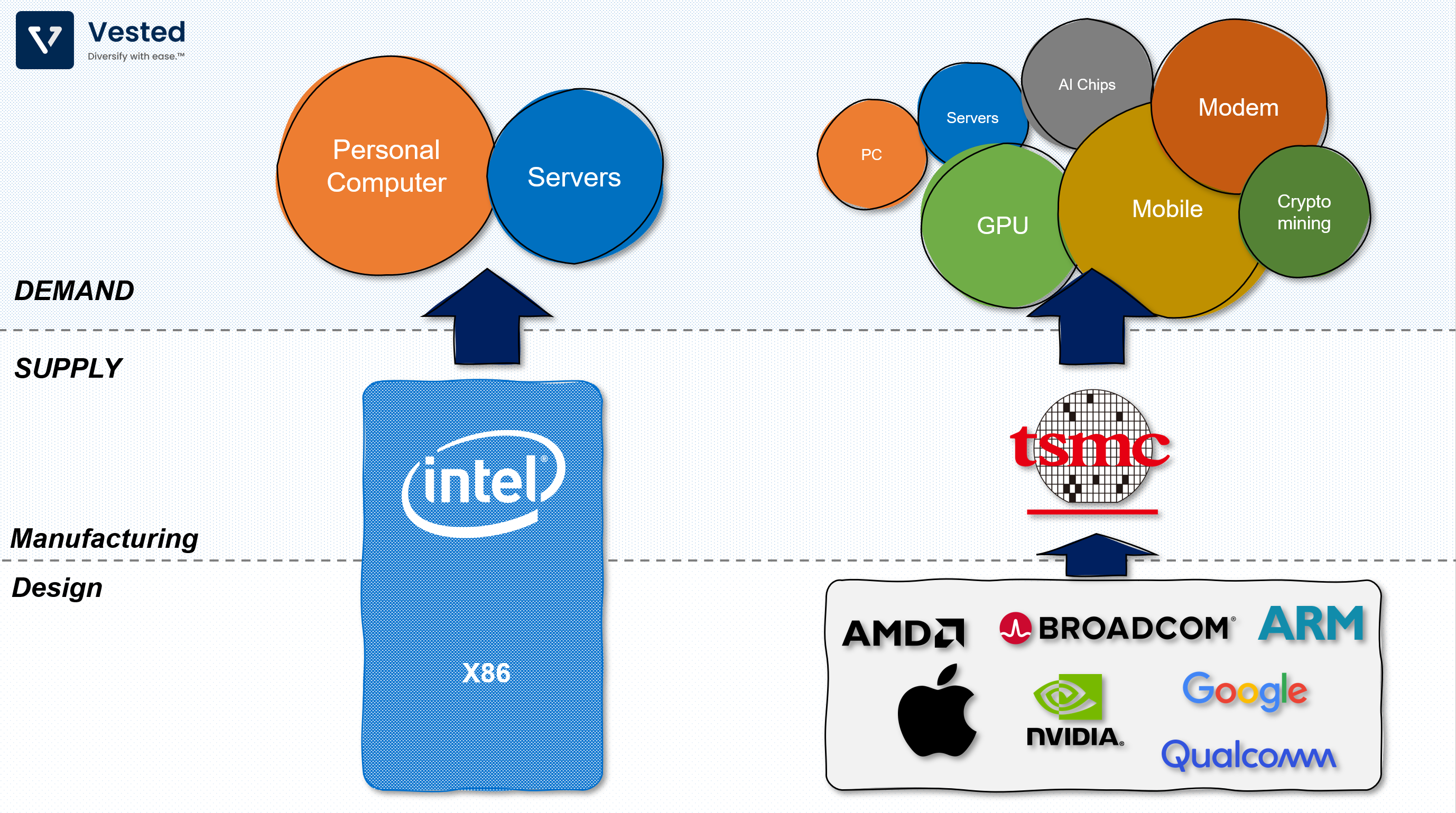

Unlike TSMC, Intel is an integrated device manufacturer (IDM). Intel designs (the x86 architecture) and manufactures its own chips. In contrast, TSM is a pure play foundry. It helps other fabless (factoryless) chip companies manufacture their designs.

This business model removed the required capital expenditures of starting a chip company, and significantly lowered the barrier of entry in the semiconductor space.

For decades, however, Intel held a manufacturing advantage over TSMC. Even in 2014, Intel had a manufacturing lead of 2 to 3 years ahead of TSMC. This meant that Intel-made chips were typically higher power/performance than TSMC-made chips. But in the past few years, Intel’s lead disappeared. The shift has had profound implications on Intel and companies that compete against Intel.

Today, TSMC has surpassed Intel in its ability to manufacture the most advanced chip node. While Intel is currently producing the 10nm node in high volumes, TSMC has deployed its 5nm node that is being used in the most advanced applications (the latest iPhones, NVIDIA’s GPUs, AMD’s server chips, and others).

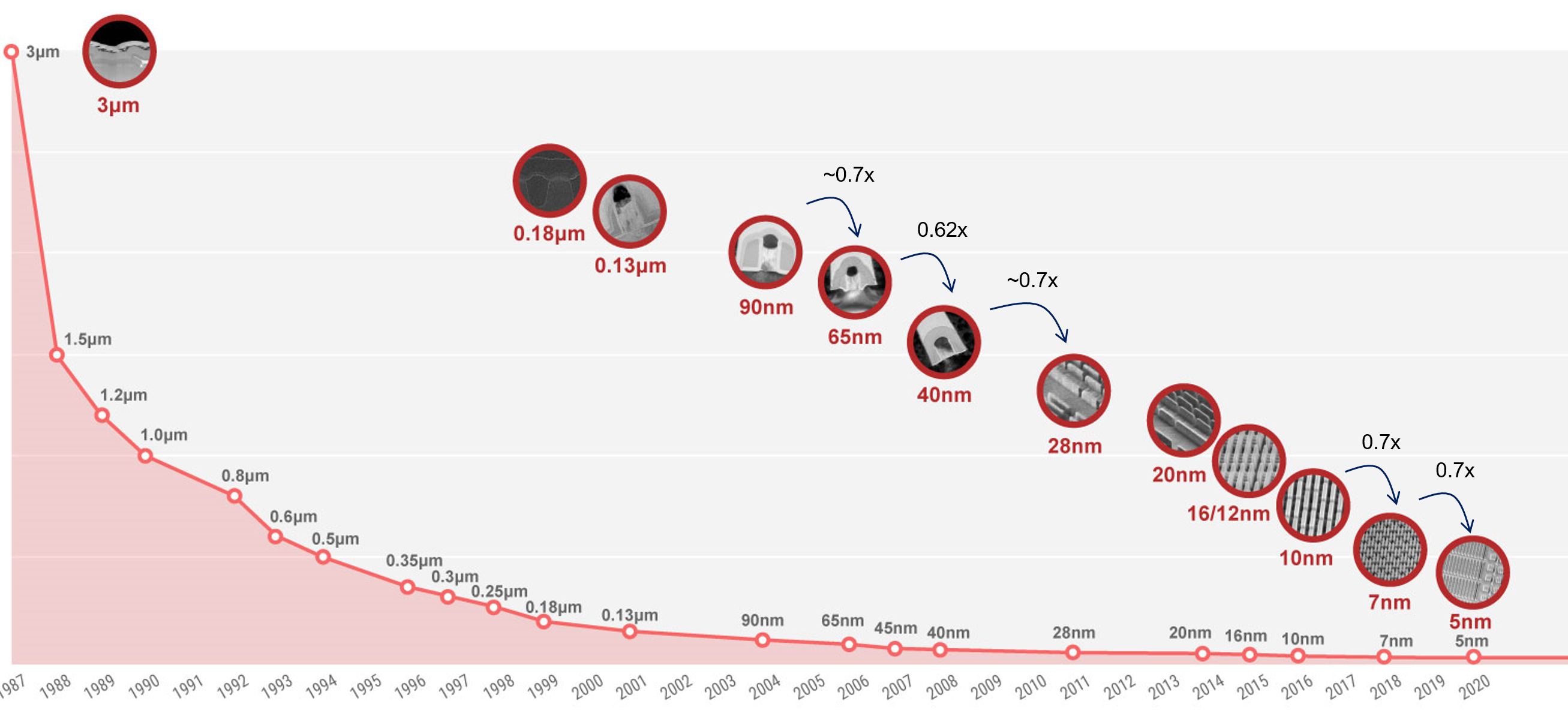

Before we go further, it is important to recognize that these technology nodes are rough approximations of transistor density. It’s more of a marketing nomenclature to identify reduction in scaling, and does not provide a perfect performance comparison. For example, Intel’s 10nm node is close in performance to TSMC’s 7nm. The numbers also do not translate to the unit length of the 3D transistors. So, you might be asking, what do the numbers mean?

Think about these numbers as convenient shorthands. Recall that Moore’s law states that the number of transistors should double every two years. A doubling in transistor count translates to a halving of the surface area of the chip.

Imagine you have a square with unit length of 1. The area is then 1 unit square (1 x 1). If you want to shrink the area by half, then you reduce the unit length by roughly a factor of 0.7 (0.7 x 0.7 = 0.49, which rounds to half). So if you have a 10nm chip node, and you double the transistor count (by shrinking the area of the chip in half), then you shrink the unit length by 0.7, which gives you: 10nm x 0.7 = 7nm. That’s where the name comes from.

Despite the nomenclature mismatch, it is without a doubt that TSMC’s manufacturing design is currently 3 to 5 years ahead of Intel, and that benefits customers of TSMC – AMD being one of them.

AMD was left for dead

Intel and AMD share a common lineage. Both companies were started by ex-employees of Fairchild Semiconductor. After Robert Noyce and Gordon Moore left Fairchild to start Intel in 1968, Jerry Sanders and his colleagues followed suit and started AMD in May 1969.

A shared lineage is not the only thing that the two companies shared. In 1978, Intel developed the x86 architecture, a design system that is still dominant in PCs and servers today. Three years later, when IBM was looking for chips for its PC, it chose Intel to design and manufacture the CPU. But the deal came with one condition – there had to be a second source manufacturer. In order to win the IBM deal, Intel gave AMD a 10-year license to manufacture the x86 design. This agreement forced Intel to create its own competitor.

So of course, over the years, Intel tried to nullify AMD’s hold on x86, resulting in multiple legal disputes between the two companies. Fast forward to today, AMD is the only other company that is capable of designing high-end x86 chips.

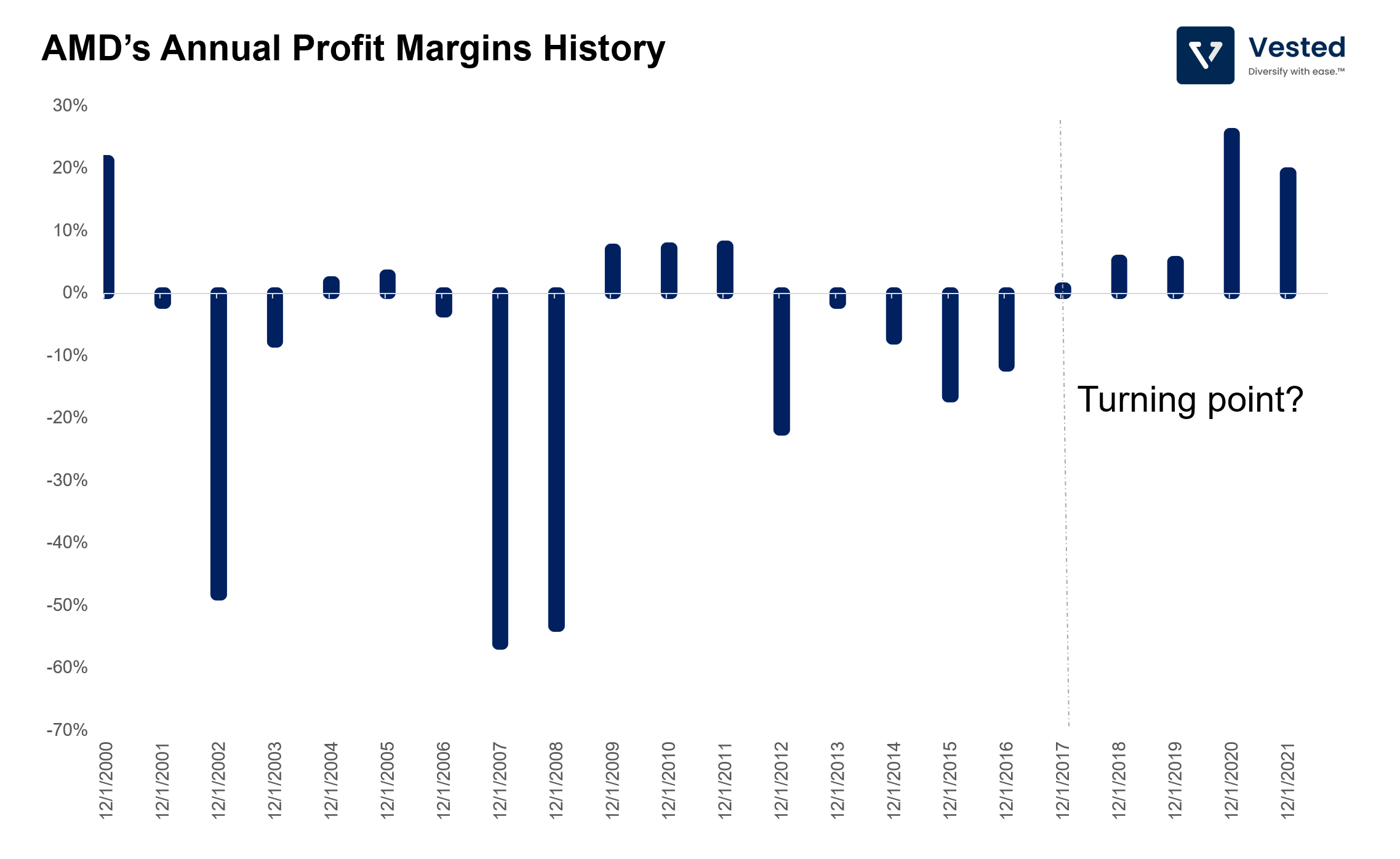

But having the capability to compete on design with Intel is not sufficient. Recall that Intel is an IDM – its designs were made by its superior manufacturing capabilities. During the 90s and the 2000s, AMD was not able to significantly win market share. And having sold its foundry business to stem losses in 2008, the company could not out manufacture Intel. The popular opinion at the time was that AMD was going to go bankrupt. By 2015, AMD’s share price was trading below $1.80/share.

As you can see in AMD’s annual Net Profit trends below (Figure 3 below), things were quite dire between 2012 to 2016. But the company seemed to turn a corner in 2017. After 5 years of unprofitability, AMD became profitable again.

It’s no coincidence that this was around the time Intel lost its manufacturing edge. After TSMC deployed its 10nm node, AMD’s products reached parity with that of Intel’s in 2017 (see Figure 4 below). But AMD’s products were priced much cheaper. By 2019, AMD’s chip servers out-performed that of Intel’s, thanks to TSMC’s 7nm process node. For the first time in decades, AMD’s design was no longer constrained by inferior manufacturing capabilities.

You can see this in the performance of AMD’s chips vs. Intel (see Figure 4 below).

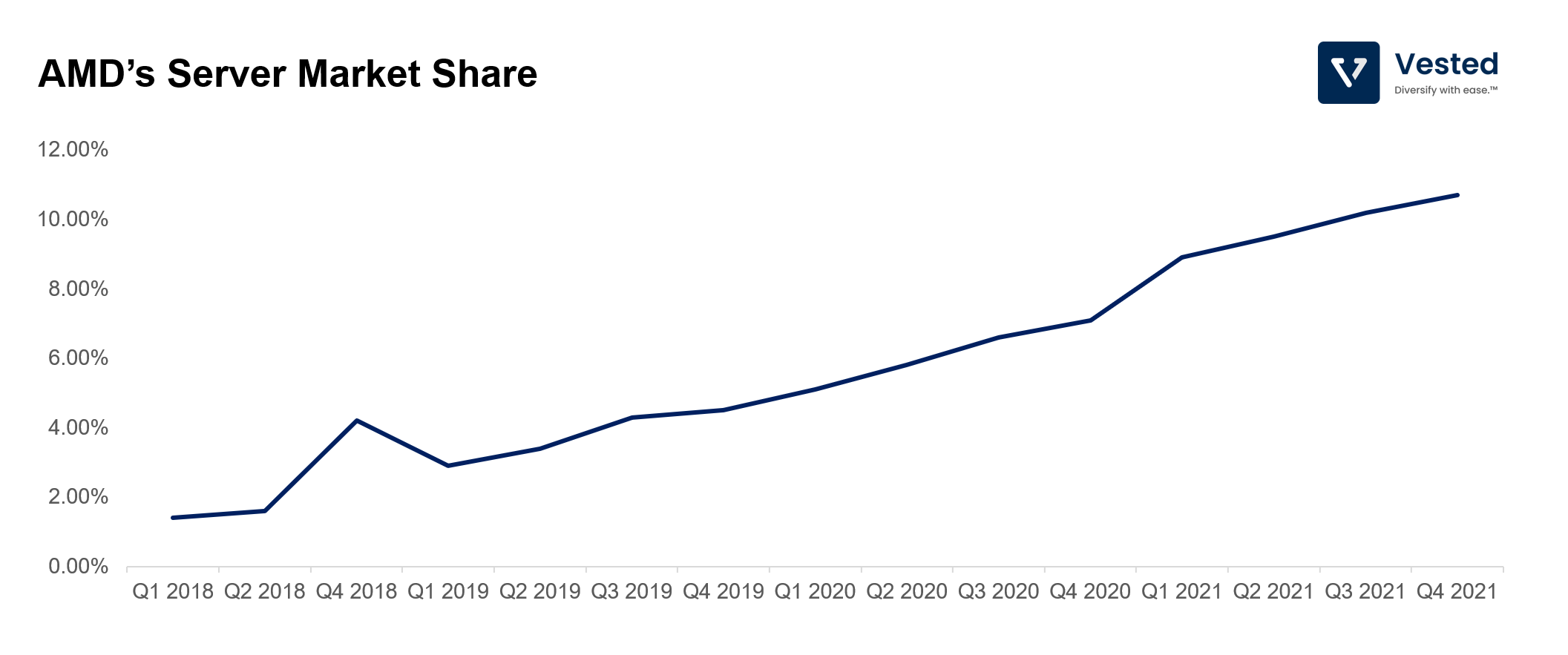

Since then, AMD continues to gain market share, especially in the lucrative server segment, at the expense of Intel (see Figure 5 below).

Apple gaining PC market share

In November 2020, Apple finally unveiled the long rumored M1 chip to be used in its desktops and laptops. It was the end of more than 15 years of partnership between Intel and Apple.

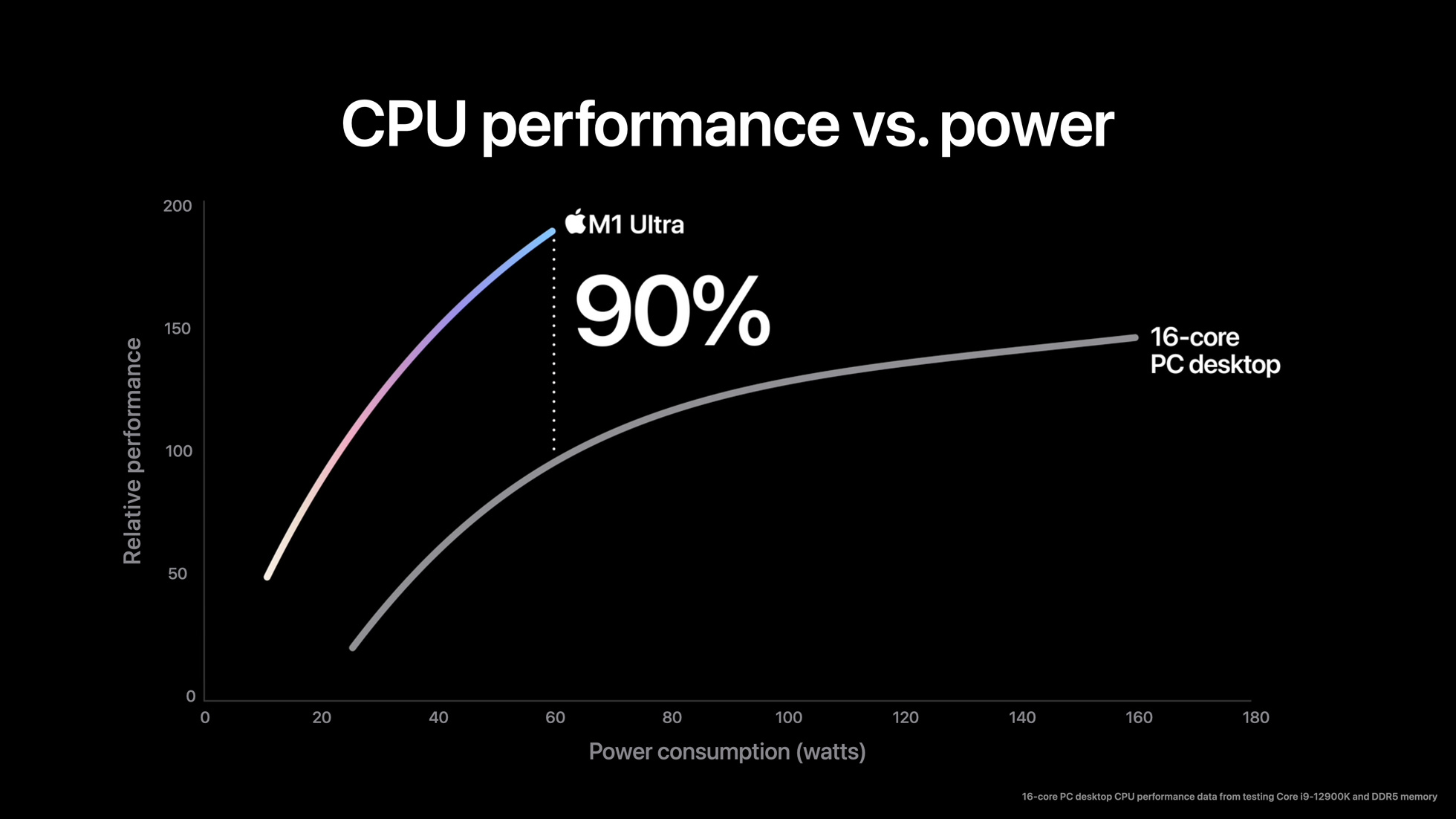

The reason Apple decided to finally leave Intel’s x86 architecture and use its own design was largely because of the same reason AMD was outperforming Intel. TSMC’s manufacturing capabilities could now unleash the full potential of Apple’s design. The result was undeniable: Apple’s M1 chip now outperforms Intel’s (Figure 5 below).

So what happened? How did Intel lose its mojo?

There are several reasons. The first reason is volume. In semiconductor manufacturing, production volume is key.

There have been many companies that lost market share, lost volume, entered a death spiral, and gave up on chip making altogether. IBM got out of the game in 2014 when it sold its chip business to Global Foundries in 2014 (for a paltry $1.5 billion). Global Foundry itself was spun out of AMD in 2008, as AMD decided to shed the unprofitable business.

These companies got outmuscled by Intel, who at the time had a dominant market share in extremely profitable chips for computers and servers segments. It was then natural for Apple, in 2015, as it was developing the iPhone, to approach Intel to help it design and produce the chip. But Intel decided to pass because of the low potential profits:

“The thing you have to remember is that this was before the iPhone was introduced and no one knew what the iPhone would do… At the end of the day, there was a chip that they were interested in that they wanted to pay a certain price for and not a nickel more and that price was below our forecasted cost. I couldn’t see it. It wasn’t one of these things you can make up on volume. And in hindsight, the forecasted cost was wrong and the volume was 100x what anyone thought.” — Paul Otellini, CEO of Intel, in 2013.

This is a classic example of low end disruption. Intel was not willing to make the necessary investments to produce low-margin chips. It turned out, their projections for volumes were way off, and as a result, Intel missed the shift to the next compute platform. At the end of 2021, the total shipment of smartphones exceeded 1.4 billion units. In contrast, PC sales were about 344 million units for the same time period.

Volume is important because of two things:

- High volume chip making has relatively zero marginal costs, but extremely high fixed costs. The initial capital expenditures to build new factories (which you have to do for every new technology node) and the years of R&D (which now stretches to 4+ years) are now in the tens of billions. As such, the higher the volume, the more you can spread out the high fixed cost investments.

- Higher volume translates to faster learning. One unique thing about chip production is that every technology node poses different manufacturing challenges. Each company has to re-learn how to make the new chips in a consistent and efficient manner. It is one thing to create a one-off chip in a lab, it’s a whole different ball game to create a process that produces millions of chips in a profitable manner. Having large volume commitment from a customer such as Apple has allowed TSMC to achieve efficient high volume manufacturing faster.

In other words, the more chips you make, the faster your learning curve to achieve high volume manufacturing, the more profitable each chip can be, the more research and development you can invest for future node production. It’s a virtuous cycle.

The second reason is technology choice. As explained by Gavin Baker in his blog, when Intel developed the 10nm node, it chose to continue to rely heavily on multi patterning using deep ultraviolet (DUV). This turned out to be a mistake. The implementation challenges associated with applying this approach on 10nm delayed Intel’s launch by 4 years. Meanwhile, TSMC decided to go with EUV, which ended up being the correct approach.

By the time Intel launched its 10nm, TSMC had begun deploying its 5nm node, 2 technology nodes ahead of Intel. Meanwhile, as of this writing, Intel’s 7nm has yet to launch (it’s been delayed by 2 years and has been slated to be released in 2023).

So now, Intel is playing catch up. It has begun inserting EUV technology into its manufacturing processes, and even contracted TSMC for the 3nm node.

The rise of fabless chip companies

When TSMC came to the scene in 1987, it was the first pure play foundry business. It didn’t make its own products. At first, there were no fabless chip companies, so TSMC had to earn a living by providing manufacturing service for other IDMs who needed extra capacity. This meant TSMC’s business grew slowly at first. But over time, it accelerated. TSMC significantly reduced the cost of starting chip companies. By its existence, it allowed three guys in a proverbial garage to launch a 3D graphics company (NVIDIA and many others).

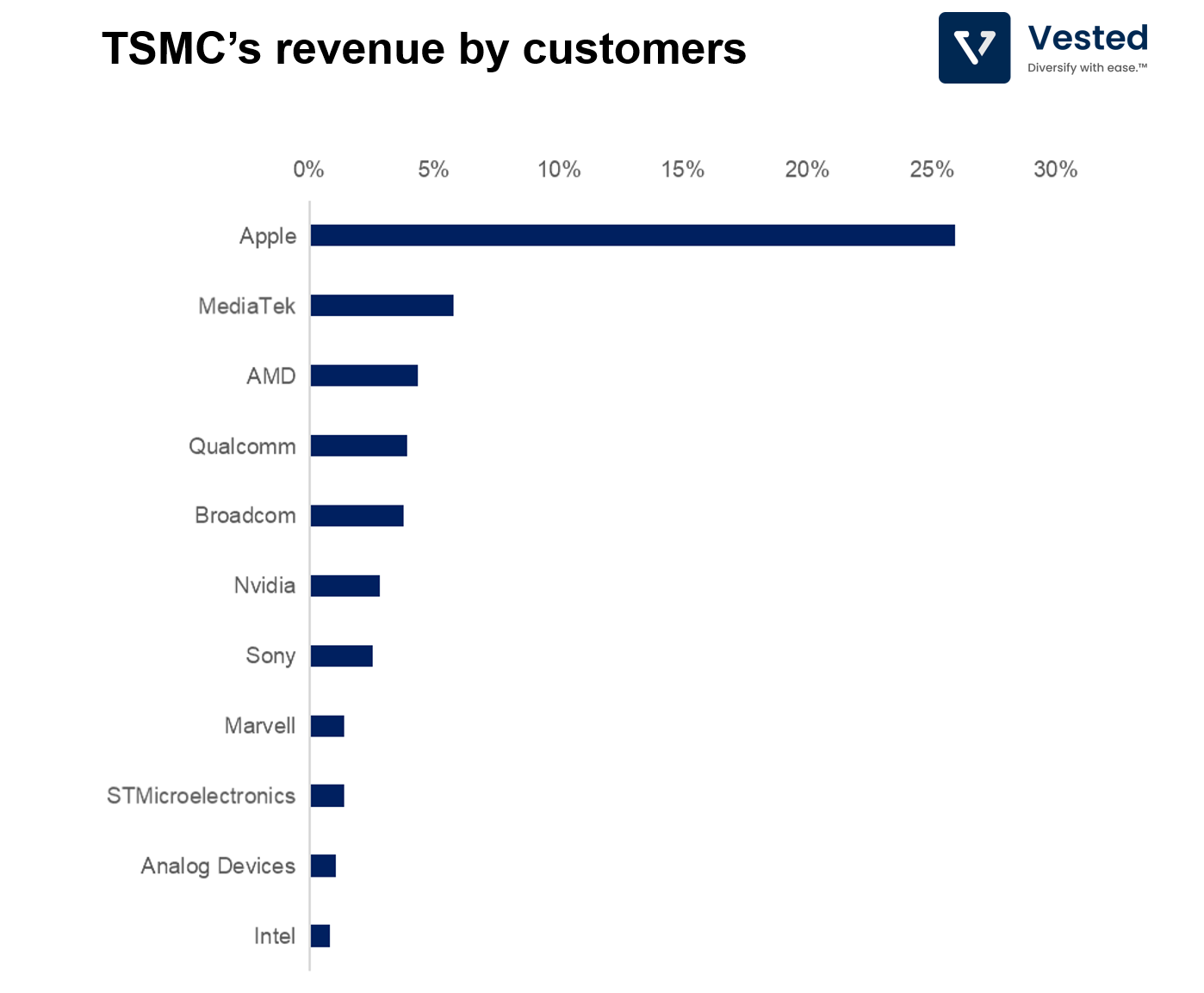

In 2021, TSMC made more than $57 billion from the following fabless companies (see Figure 6 below).

What TSMC has accomplished is nothing short of amazing. When it first started, there was no semiconductor industry outside the large fabs in the US and Japan. There was no such thing as fabless design companies. Although it took multiple decades to do, TSMC perfected the pure play foundry model. They even surpassed Intel in manufacturing ability. All it took was a paradigm shift in compute platform, a bit of luck, and a high level of discipline.

Let me close this article with one final story. A year or so into my tenure at Intel, we heard rumors that in order to catch up to Intel, TSMC instituted a 24×7 R&D rotation (mind you, 24×7 work schedule for PhD scientists to do research, which is very uncommon – this type of non-stop coverage is more common for production). While we worked hard at Intel in the development team, the research team did not work 24 hours. This was the level of discipline that was required to achieve the impossible, and as TSMC increases its presence in the US, some of these cultural exports are clashing with the US culture.

“Basically, one machine does not require a Ph.D to look after it,…†“… But since we have these over-educated engineers managing the process, they can deal with problems onsite very quickly. That’s how the competitiveness of TSMC really emerged.

“We are fielding our Ph.Ds as foot soldiers, but actually many of them could be colonels. That kind of culture wouldn’t work in the United States.†— Lai I-Chung, president of The Prospect Foundation, a think tank run by the Taiwan government.