Skip to content

Skip to content

Path to Economic Recovery

We’re entering the 3rd month of the global lockdown and many countries are re-opening. This week, we dissect the macroeconomic data of various countries to gain a better understanding of each country’s path to recovery, as well as the recovery across sectors. This piece is data-intensive as we look into:

- Supply-side economic indicators: Manufacturing and services sectors

- Demand-side economic indicators: Consumer spending through physical and digital commerce

Supply Side Recovery

As countries slowly reopen, we can gauge the pace of supply side recovery using Markit’s Purchasing Managers’ Index (PMI), a survey conducted on private corporations worldwide to measure business conditions.

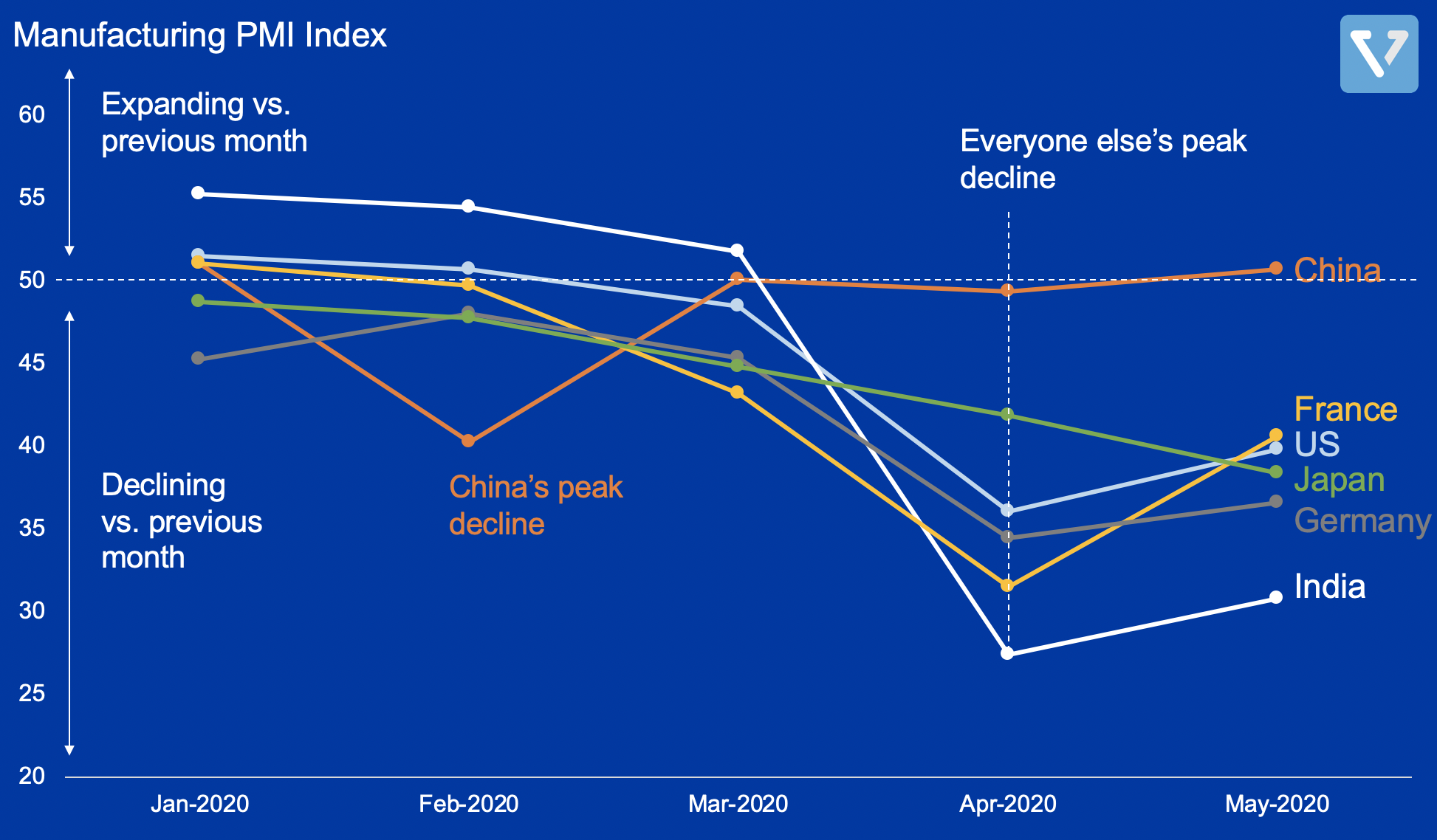

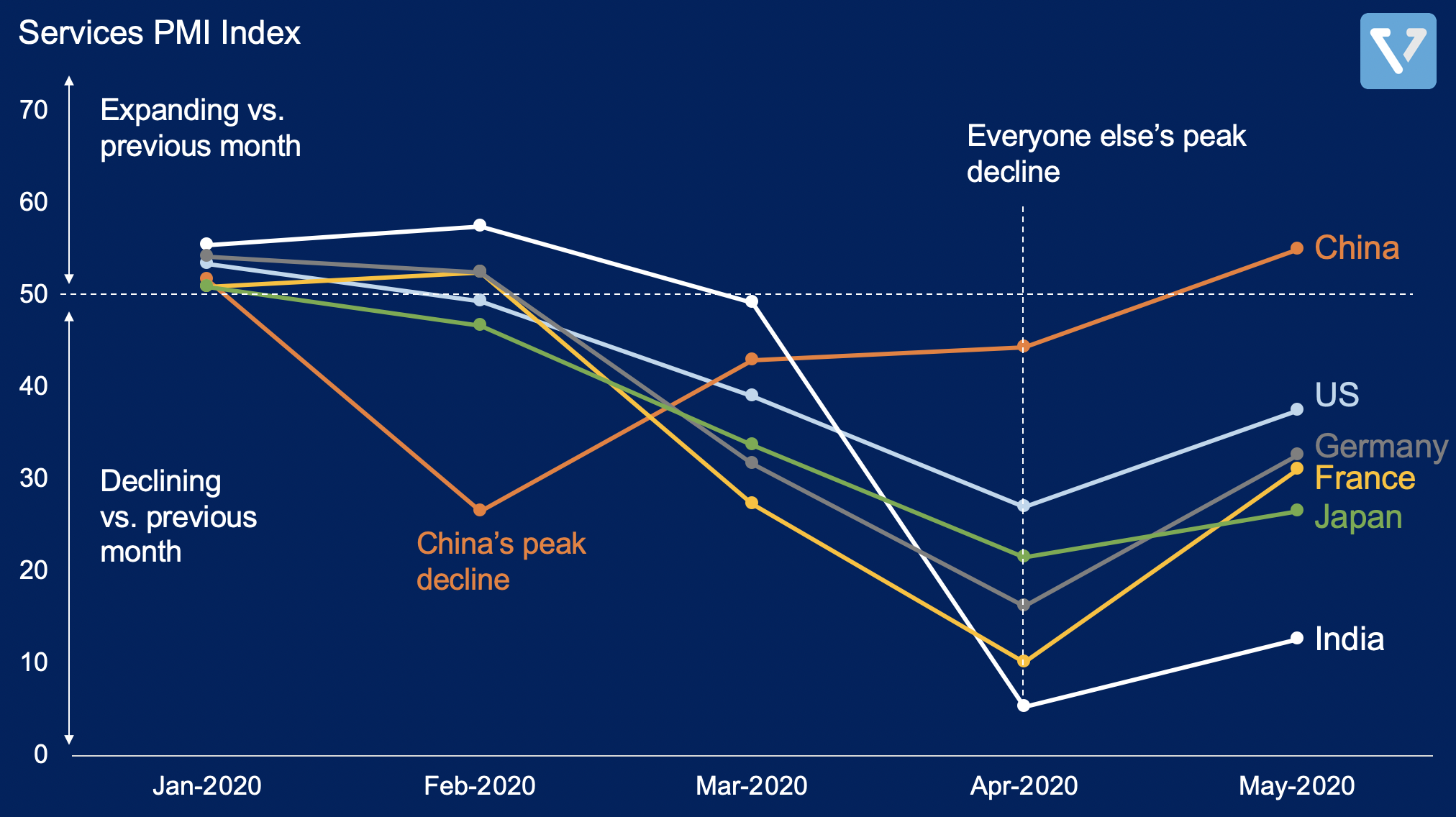

At a high level, the supply side of the economy can be further broken down into two categories: manufacturing and services. In Figure 1, we show the Manufacturing PMI of several of the largest economies in the world (US, China, India, Japan, Germany, and France). In Figure 2, we show the index for Services.

Note: PMI is a normalized index. Index value > 50 means that the specific economic activity is growing when compared to the previous month. Conversely, if the index value is < 50, the specific economic activity is contracting when compared to the previous month.

Figure 1: Manufacturing index of US, China, India, Japan, Germany, and France

Figure 2: Services index of US, China, India, Japan, Germany, and France

Key takeaways:

- As expected, China is ~2 months ahead of the recovery curve compared to the other countries because it went into lockdown 1 – 2 months earlier. China saw the steepest decline in both services and manufacturing activities in February. Meanwhile, April was the worst month for the US, India, Japan, Germany, and France. For China, this is a double whammy – as its manufacturing was ramping up, the global demand for its goods declined as the rest of the world went into lockdown.

- Services are taking longer to rebound than manufacturing. As seen in China’s curve in Figure 1, the manufacturing index rebounded to 50 within one month. However, Figure 2 shows that the services index took 2 months before crossing 50 (as always, when looking at the Chinese macro data, take it with a grain of salt, as the country has a habit of exaggerating economic data).

- For both manufacturing and services, India is experiencing the steepest decline (from March to April) and the slowest rebound (from April to May). This pain is experienced in many sectors, but the worst hit sector might be automotive. In April of 2020, not a single new car was sold in the country. The lockdown is costing the industry an estimated US $306 million per day.

Demand Side Recovery

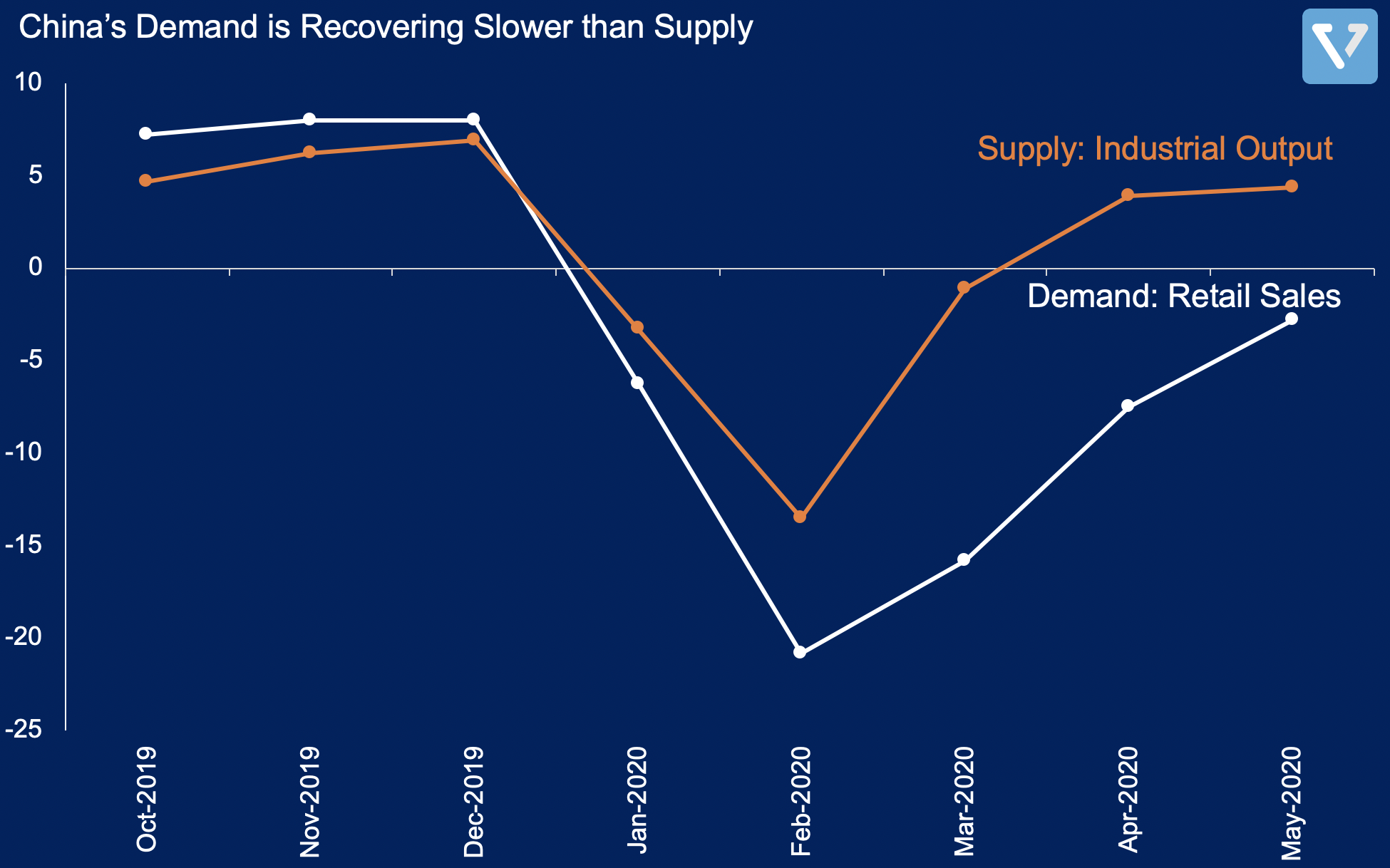

Between supply and demand, recovery of the supply side is likely to be faster. The supply side needs revenue as a matter of survival and will reorganize itself rapidly to adapt to the new COVID environment. You can see this phenomenon in China; while industrial output has mostly recovered, weak domestic and international demand are constraining demand side recovery (Figure 3).

Figure 3: China’s year-over-year growth/contraction of factory output and retail sales. Data was sourced from National Bureau of Statistics by Bloomberg

Meanwhile in the US, despite record unemployment numbers, consumer sentiment and spending is on the rise. Economists at Goldman Sachs estimate that consumer spending is back at 90% of pre-pandemic level (up from 74% in April). Consumer spending is a very important factor in the US economy, as it contributes towards about 70% of US GDP.

If consumers are spending, the question then becomes: “Are consumers spending through digital or physical commerce?â€

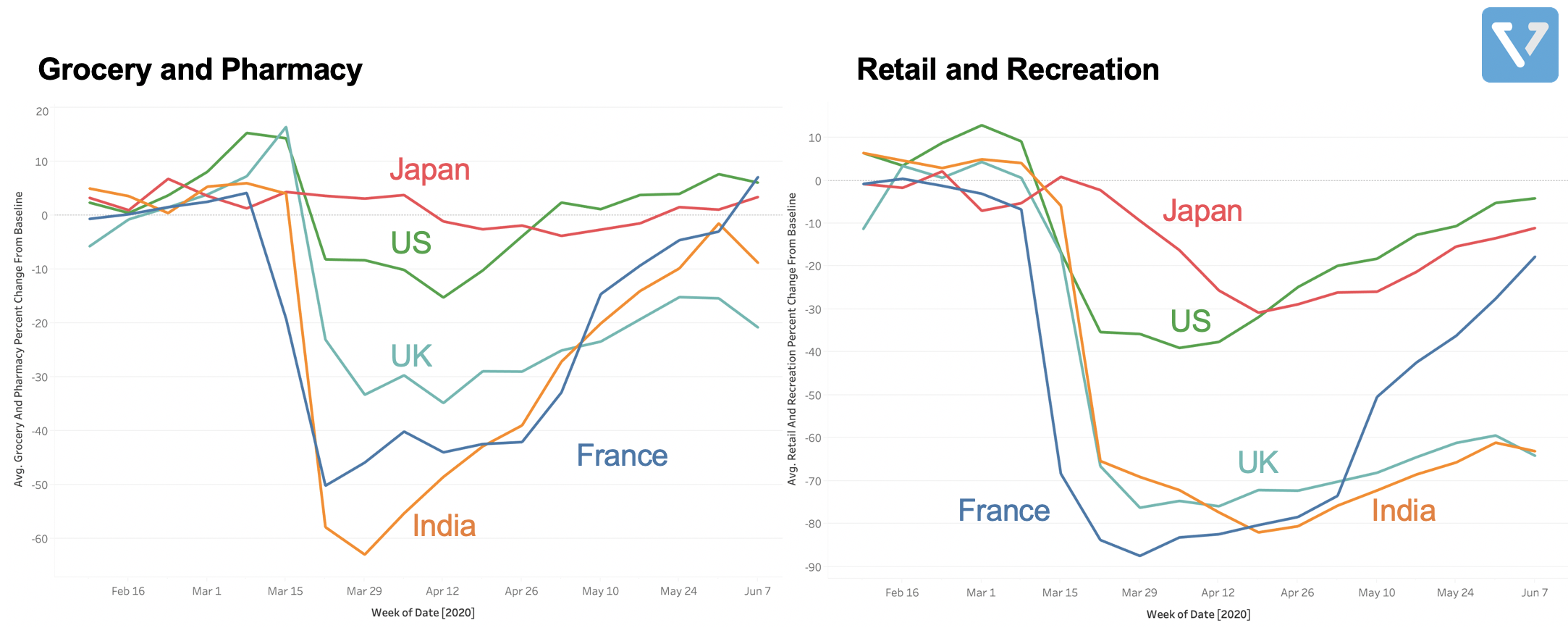

Physical travel declined by as much as 90% in India and France due to the lockdown. Using Google’s community mobility data, we can gauge the relative change of physical travel for two key categories: (1) essentials (grocery and pharmacy) and (2) non-essentials (retail and recreation). As you can see in Figure 4, the mobility trend in Japan remained relatively constant since the country did not impose stringent lockdown measures. Nonetheless, travel to retail and recreation sites declined – which negatively impacted the economy.

Figure 4: Google’s community mobility report (source)

What does this mean for recovery across sectors?

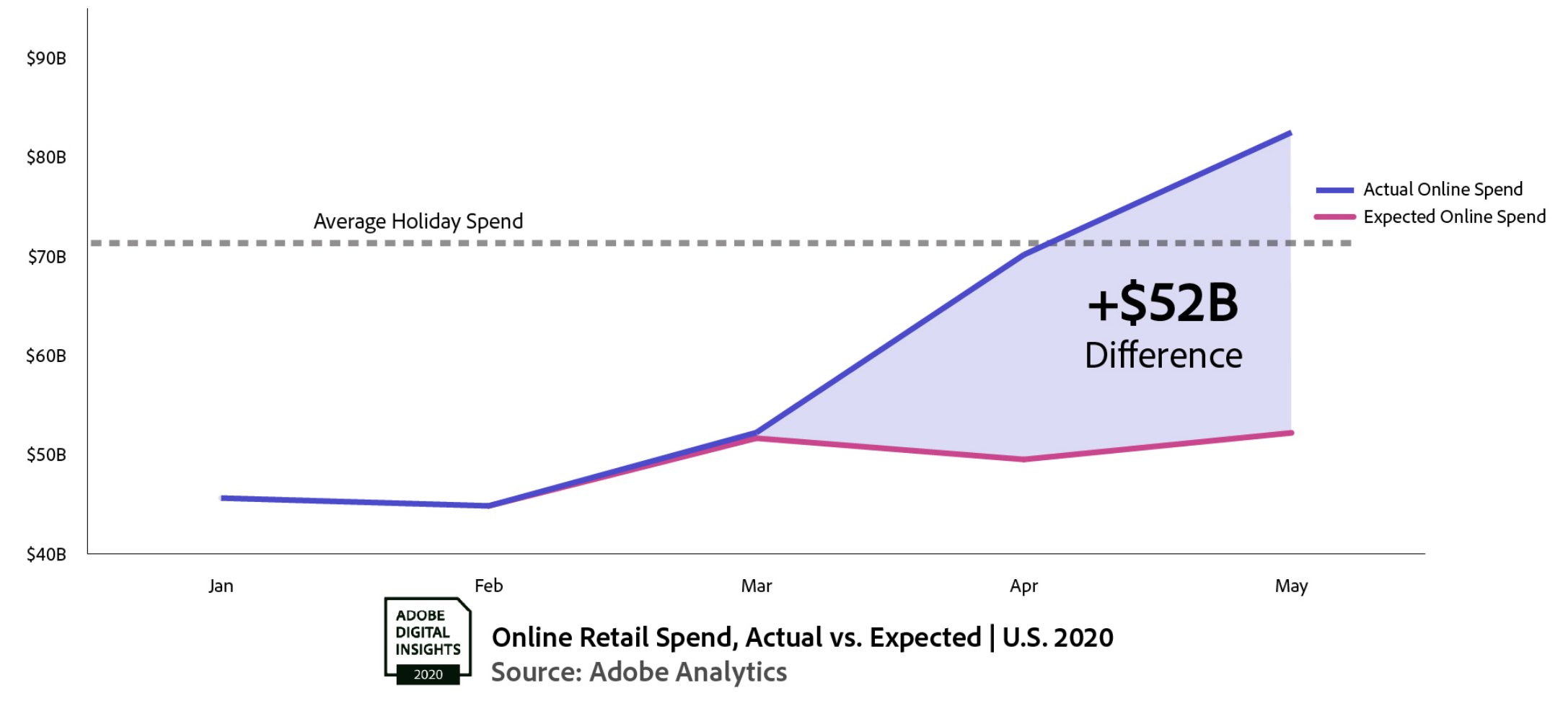

Since consumers are unable to travel, the online channel is absorbing the offline retail economy. In the US, e-commerce gained an additional US $52 billion in spend during the lockdown. That is a whooping 78% increase in May compared to the same period a year ago. It is likely that this trend is observed globally.

Figure 5: E-commerce gained an additional US $52 billion in extra spend during the lockdown. Data from Adobe Analytics

But the economy cannot survive on digital alone. So then the next pertinent question when thinking about recovery is: When will physical retail recover? This is much harder to answer. There are some signs of recovery in the US (US retail increased by 17.7% in May compared to April), but this bounce might be a sign of recovery from a very low base and a release of pent up demand, which might not be sustainable in the long term.

What will the medium/long term look like? How will the economy return before we have a vaccine? One way to imagine a post-lockdown world is to imagine COVID-19 as a tax to the economy – where the payment is either you getting sick or dying (sorry, we just turned morbid here, but bear with me).

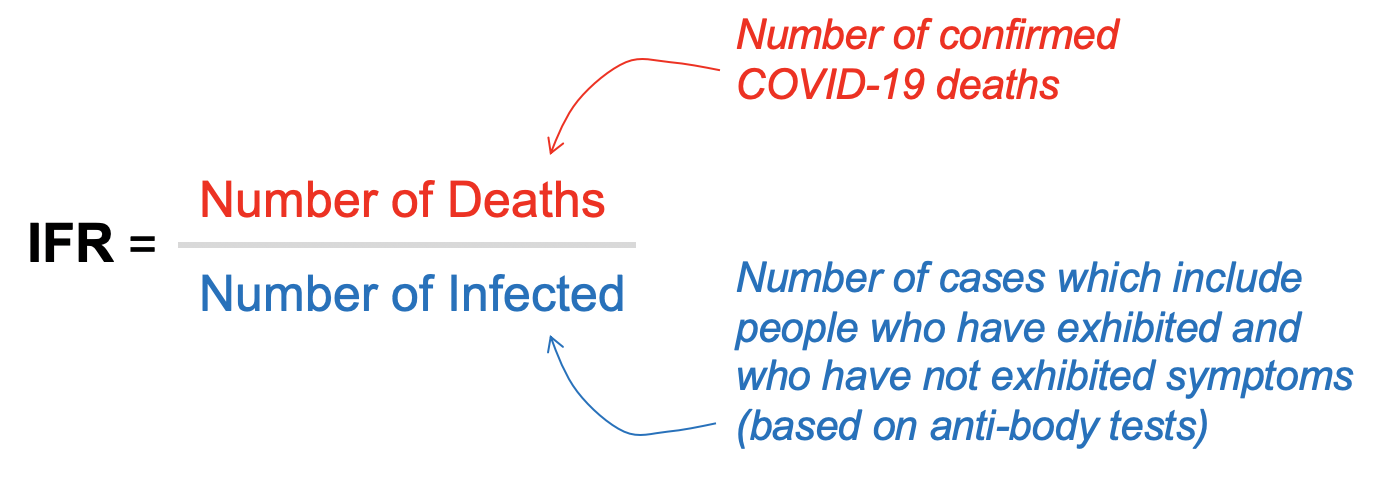

How do we determine this tax rate? For this, we can estimate using the Infection Fatality Rate (IFR). The IFR is the ratio of the official counts of people who died from COVID-19 to the total infected with COVID-19.

Figure 6: Calculating IFR

From this meta-analysis, it seems likely that the IFR is around 0.5% – 1.5%. Let’s take the lower number of 0.5%. This means, assuming that everyone is a rational actor, every economic activity is weighed down by the 0.5% possibility of death. As such, only certain ‘must do‘ activities will resume to previous levels, for instance:

- It might not be worth it to go to a crowded stadium to watch a concert / fly for a vacation / in-person business meeting given there’s a 0.5% chance of death

- But it might be worth it to brave the 0.5% risk of death if my livelihood (ability to pay rent, put food on the table) depends on it

This is why the US Fed Chief Jeremy Powell believes that the recovery will be in three phases: (1) shut down, (2) rapid bounce back, and (3) return to a level of activity that is lower than before the pandemic. We just entered phase 2, and it is unlikely that we pass phase 3 without a vaccine.

As an investor in the financial market, what does this mean for you?

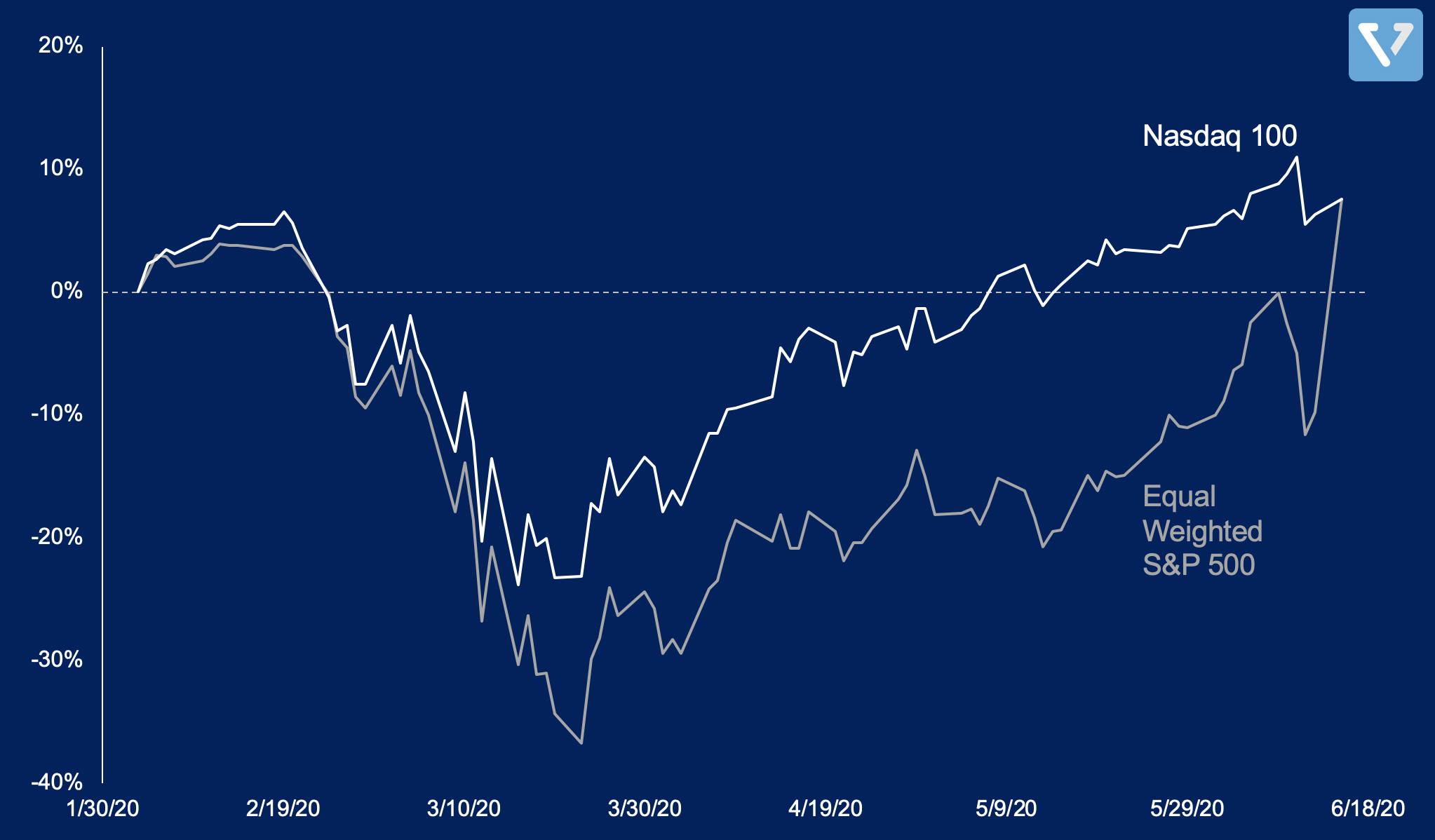

If you’re wondering which country or sector to invest in, or which will have the fastest path to recovery, then perhaps the more apt question is: Which sector has experienced minimal disruption during the lockdown and can be more resilient towards a potential 2nd wave of COVID-19? Which sector is experiencing faster adoption because of the pandemic?The answer to these questions is the Technology Sector (see Figure 7).

So far, US stock market recovery has been uneven, but the technology sector (Nasdaq) has recovered much faster and experienced less decline than the overall market. In Figure 7, we use the equal weighted S&P 500 index as a representation of the broader market (instead of the traditional market cap weighted S&P 500 to mute the effect of big tech).

Figure 7: US stock market recovery has been uneven, but the technology sector (Nasdaq) has recovered much faster and experienced less decline than the overall market. We use the equal weighted S&P 500 index as a representation of the broader market. This index has the same constituent as the normal S&P 500, but each company only has a weight of about 0.2% (in contrast to the standard market cap weighted S&P 500 that is heavily dominated by big tech)