Skip to content

Skip to content

In today’s article, we discuss Netflix’s Q4 2020 earnings, and how Amazon and Disney competes against Netflix.

Netflix announced its Q4 2020 earnings and its shares popped

Here are a few key highlights from Netflix’s Q4 2020 earnings announcement:

- Paying subscriber base crossed 200 million (203.66 million subscribers) after adding 8.51 million net new subscribers globally.

- 83% of new subscribers in 2020 came from outside the US and Canada, where Netflix has saturated the market and is facing stiffer competition.

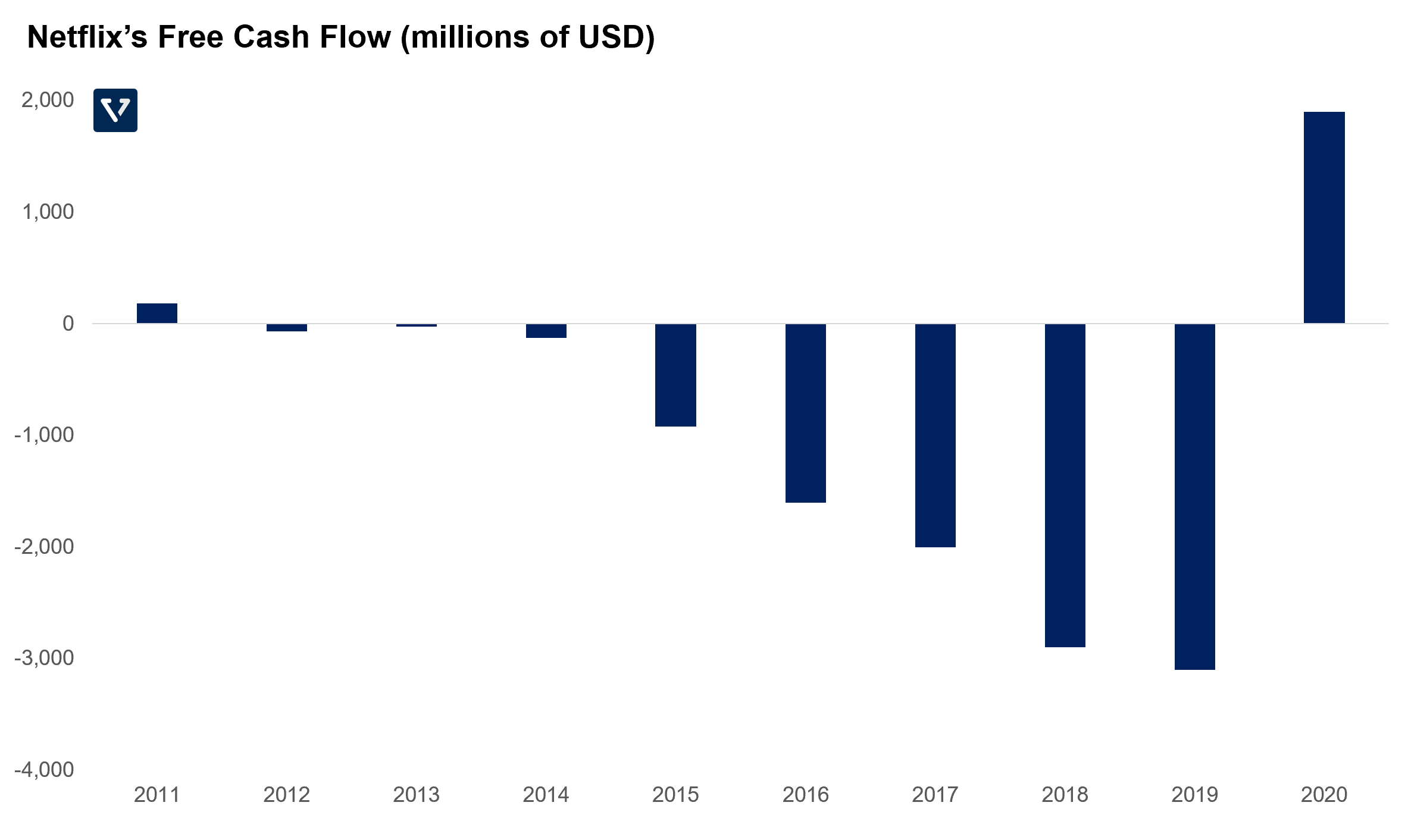

- The biggest revelation from this announcement is that the company has achieved positive free cash flow (FCF) in 2020 and believes that it is very close to sustainably maintaining this positive FCF moving forward. Which means that the company plans to no longer rely on debt and may restart its stock buyback program (something that it did between 2007 – 2011).

Why is this a big deal for Netflix?

One of the bear cases for Netflix is the neverending cash spend that the company carries out to fuel original content production. This cash burning strategy started around the beginning of last decade (you see the FCF turned negative around this time – see Figure 1).

Note: To raise the funds it needs to produce original content, the company could have done one of two things:

- Issue and sell more shares, dilute existing shareholders but generate fresh cash to invest in content

- Or raise cash from debt

Netflix chose debt because the company believes that debt is cheaper than issuing equity in the long run, especially in this low interest rate environment. In the past few years, it has been issuing bonds at an interest rate between 3 – 6% per year. For example, here’s a bond issued in 2015, with an annual interest rate of 5.875% per year. In contrast, over the same period, Netflix’s share price has returned about 28% CAGR.

According to the bears, this is a high risk strategy, because cost of content production and cost to acquire customers are expected to go up due to increased streaming competition from Amazon, Disney and others. And if both the costs go up and the debt comes due – Netflix may experience a cash crunch.

But with this latest earnings announcement, Netflix has signaled that it can generate enough revenue to pay down its debt, while maintaining a large content budget, without relying on debt in the future. This significantly reduces the possibility of the bear case outlined above. This is why the share price popped.

How did Netflix achieve positive Free Cash Flow in 2020?

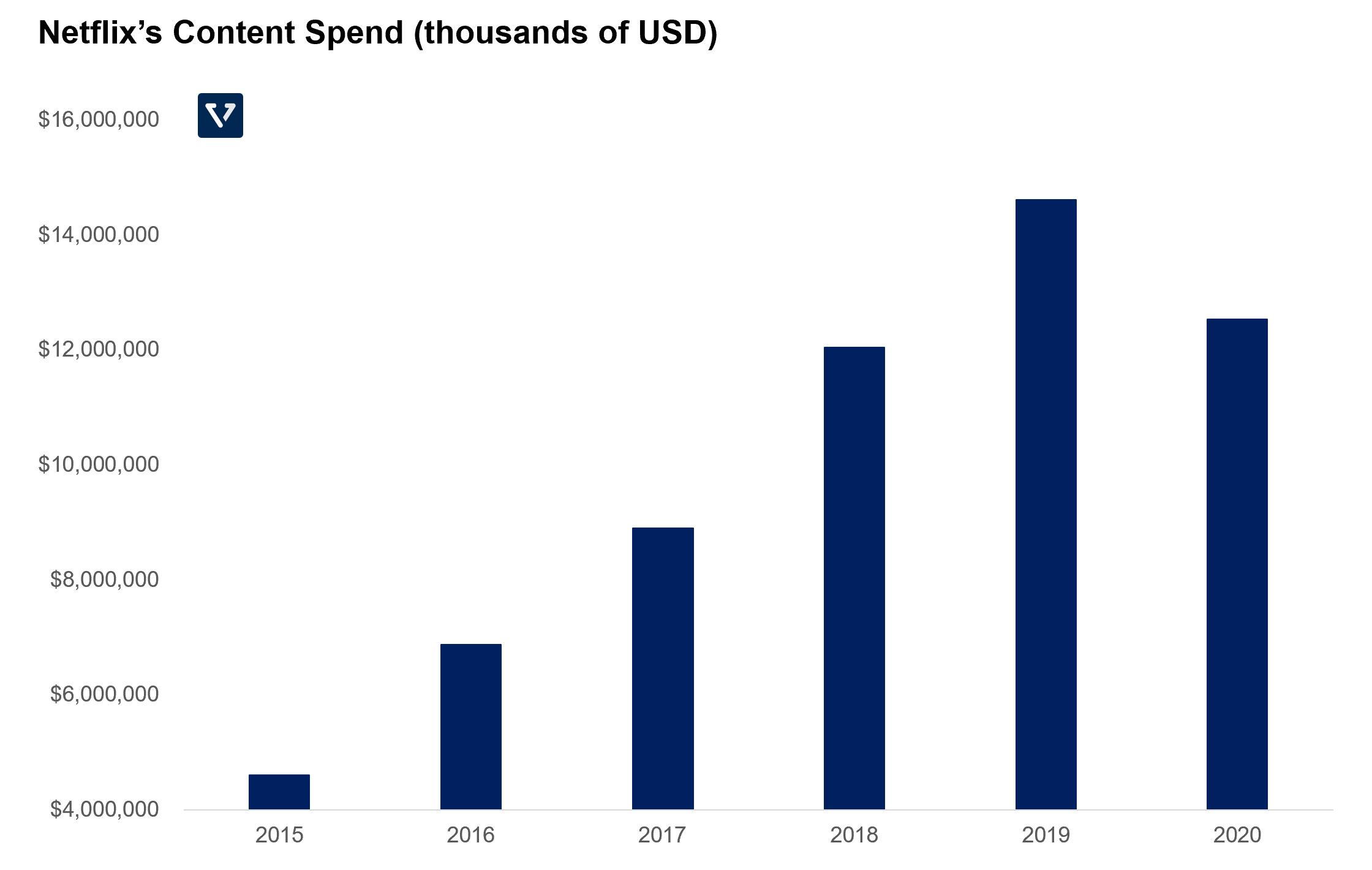

With increasing competition, Netflix was forced to spend more on content (see Figure 2), from US $4.6 billion in 2015, to more than 3X increase in 2019 (US $14.6 billion). But in 2020, because of a stoppage in production (due to the global lockdown), the spending went down to US $12.5 billion (a 14% reduction).

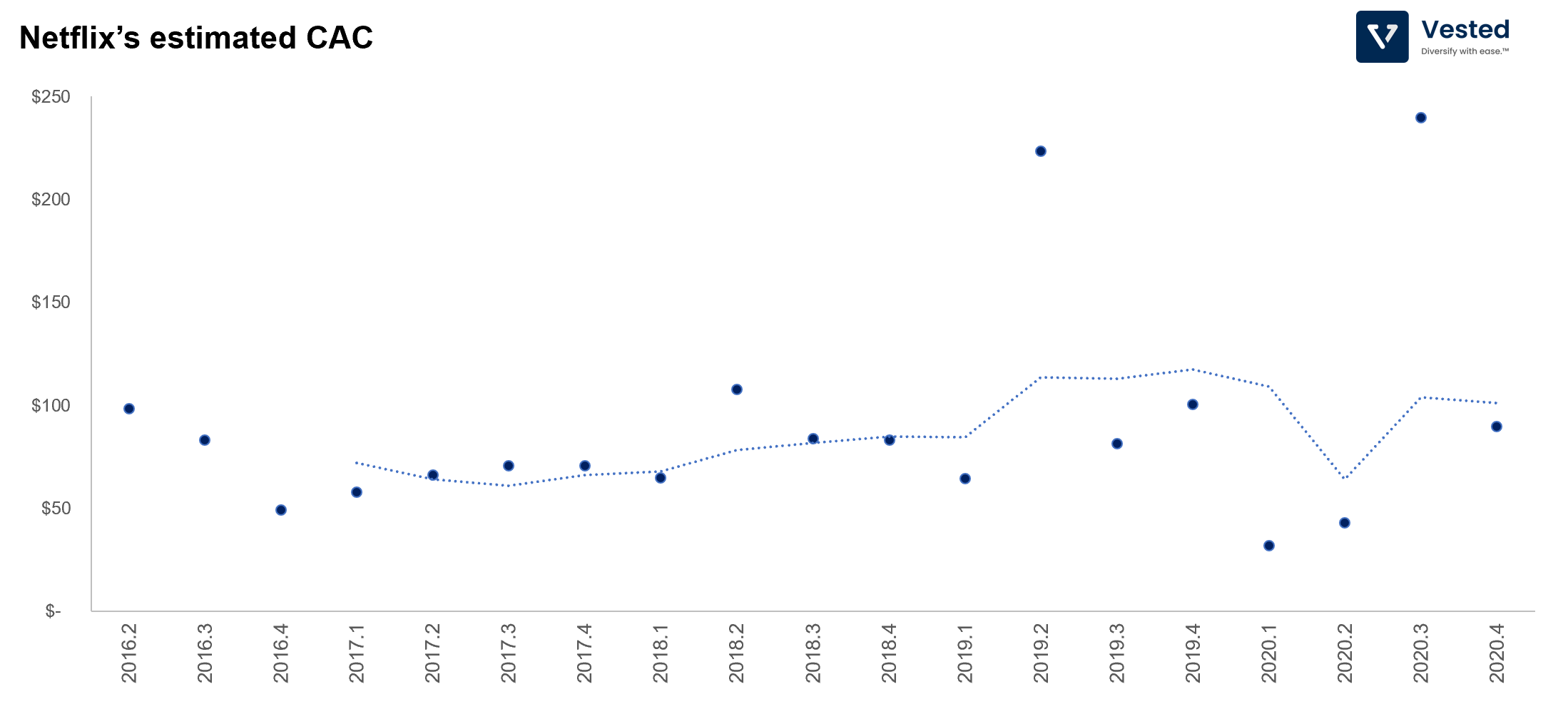

Also, due to the lockdown, customers signed up in droves, accelerating Netflix’s adoption. As a result, the company was able to reduce marketing spend but still grew faster in 2020. This translates into lower customer acquisition costs (CAC), as is shown in Figure 3.

As a result of these two things (and the accelerated revenue growth), Netflix was able to end 2020 with a positive FCF.

Is this sustainable?

Likely so. The great thing about subscriptions business is that, if you pull forward gain of paying subscribers (e.g. subscribers that would’ve subscribed next year or the year after under normal conditions are subscribing now), the impact on revenue, and therefore cash flow, is permanent.

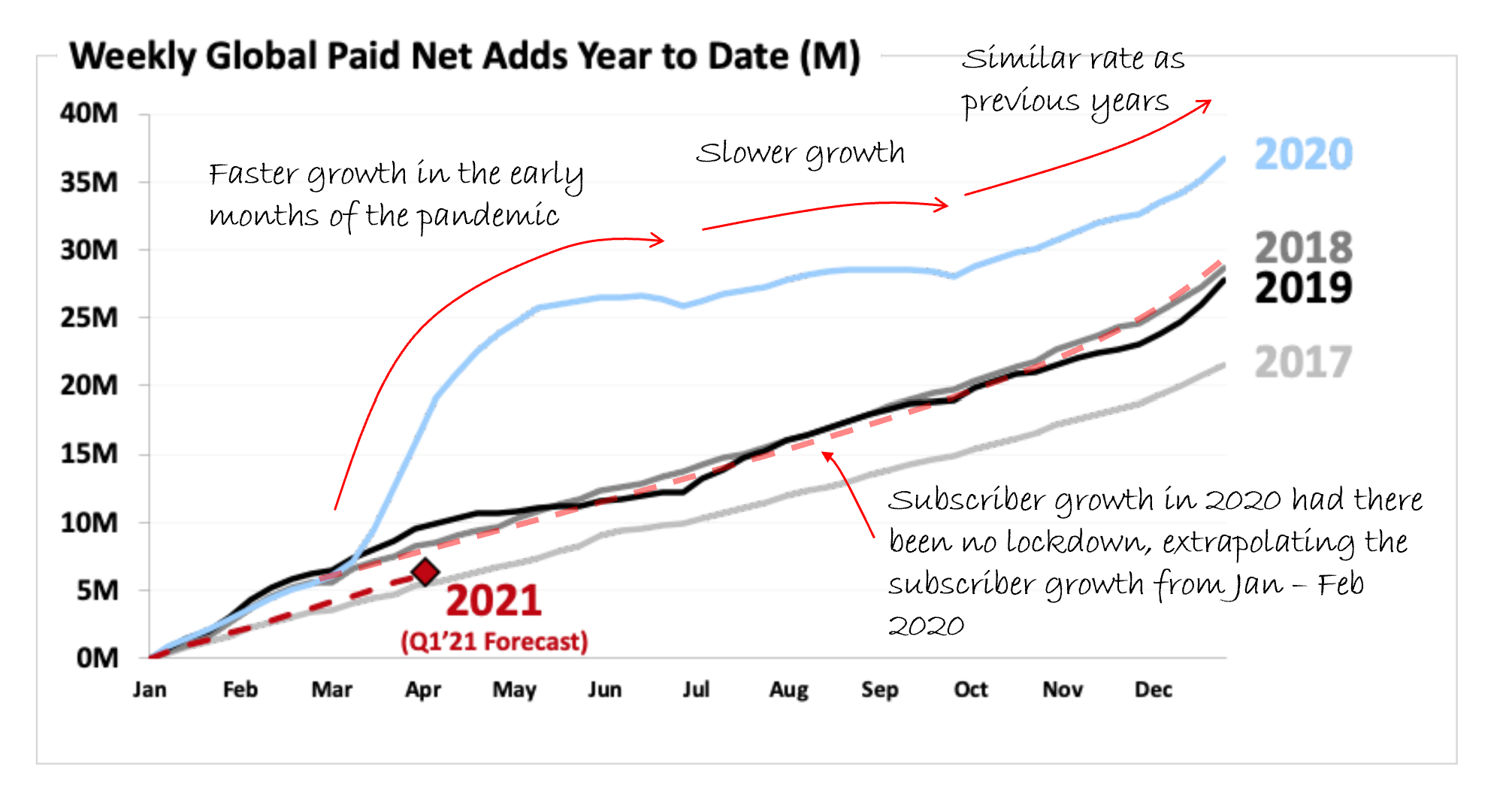

Figure 4 shows the subscriber growth rate by the years, taken from the earnings release. You can see that early in 2020 (Jan – Mar 2020), Netflix’s growth was similar to previous years. Then, after the global lockdown started in mid March, subscriber growth rate ballooned, outpacing projections. This was then followed by a slower growth in Jun – Sep 2020. But by Oct – Dec 2020, the growth rate normalized, similar to the rates of previous years.

If we extrapolate Netflix’s subscriber growth based on trajectory from Jan – Feb of 2020 (before the global lockdown) to the entire year, Netflix was likely on pace to gain net ~28 million new subscribers (red transparent dash line – our projection).

But instead, due to the global lockdown, Netflix gained 36.6 million new subscribers in 2020 (blue line).

This difference of ~8.6 million additional paying subscribers, at an annual average revenue per user (ARPU) of US $130 (for 2020), translates to more than US $1.1 billion in additional recurring revenue. This positive impact on cash flow is permanent (net of churn).

How to compete with Netflix?

Overall, for the year 2020, Netflix generated almost US $25 billion in revenue, with expanding operating margin. Its investments in original content means that:

- It can distribute the content globally without licensing complications

- It spends heavily upfront but owns the content forever – making the cost fixed cost

- Now that it has more than 200 millions paying subscribers globally, it can spread out the large fixed content investment costs (anywhere between 15 – 20 billion a year) to a large user base

- More content translates to less churn and more growth

This is the basis of Netflix’s scale-flywheel.

Does this mean no one can compete with Netflix? Not necessarily. It is difficult to challenge the company head on since it has such a scale advantage. But there are generally three strategies employed by others:

Strategy 1: The orthogonal approach – content production fueled by other businesses

Some of the best businesses in the world utilize an orthogonal business strategy, where they provide services for free/low-cost and monetize in other ways. For example: Google provides you with a free search engine, web browser, cloud documents and many other services, but makes money by monetizing your time and attention.

In the context of streaming services, Amazon’s approach is an orthogonal one. It competes with Netflix for your viewing time, but it pays for its content investments through Prime membership, advertisements, and the sale of everyday goods through its ecommerce platforms.

Since there are so many different ways that Amazon can make money from each Prime member, it can afford to spend as much on content to compete with Netflix even if its subscriber base is not as large.

Strategy 2: The differentiated content approach – have unique content

Instead of competing with Netflix on diversity of content, you can choose to compete on differentiated content.

For example, HBO Max, a streaming service owned by Warner Media (AT&T), tries to leverage its DC Comic franchise and has decided to move Wonder Woman 1984 and its entire 2021 movie slate to the streaming service (in lieu of theatrical release).

It’s still an open question whether this strategy will work for the company. The content might not be good enough (I mean, have you seen Justice League?). Also, customers may not have the budget for a 4th or 5th streaming service. As of early December, AT&T disclosed that the streaming service has a little over 12 million subscribers – a small number compared to Disney+ or Netflix.

Strategy 3: A mix of both

One company that is trying to have differentiated content and monetize via other businesses (both strategies (1) and (2)) is Disney. Disney has a long history of rich differentiated content (Star Wars, Marvel, Disney, Pixar, etc.) and legacy businesses that allow the company to compete with Netflix.

Step 1: Grow user base. Disney plans to use its streaming service to acquire and have a direct relationship with the customer.

- In October 2020, the company announced a reorganization that elevated the importance of the streaming service (Disney+) within the company, as the spearhead of user acquisition.

- It priced Disney+ to undercut its competitors (US $6.99 per month in the US), which is cheaper than the $13.99 per month for Netflix and US $14.99 per month for HBO Max.

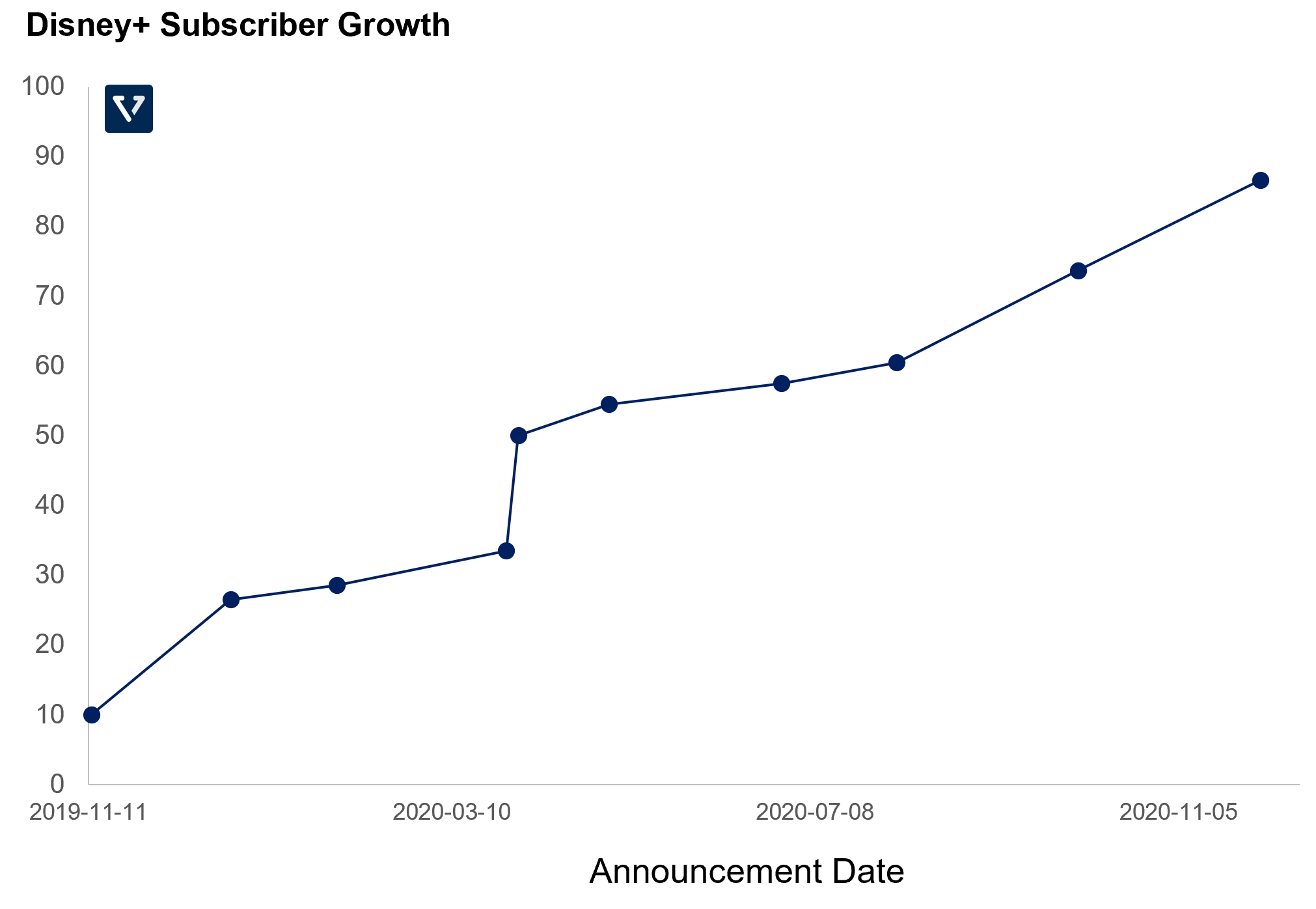

- In a little over a year, Disney+ has 86.6 million subscribers, close to half that of Netflix, and four years ahead of projections. About 30% of that is Hotstar subscribers (a leading streaming service in India).

Clearly, its strategy of differentiated content is working. Its growth is ahead of plans, and now it plans to slowly increase price (the first one to come in March 2021) – similar to what Netflix has done in the past.

Step 2: Monetize via other means.

- Through its legacy businesses, the company monetizes its franchises via merchandise sales and theme parks

Investors seem to like what they’re seeing from Disney. Recently its share price reached an all-time high, despite a significant portion of its business still being hampered by the global lockdown (Parks, Experiences and Products revenue is still down 61% in Q3 2020 compared to the same period in 2019).

What does this mean for Netflix?

Disney+ is turning into a formidable challenger to Netflix. It has the business model to compete on content investments. It has the differentiated content that people want. And it has a significant foothold in India (through Hotstar), an important growth market for Netflix.

Netflix likely will observe increased churn. The average US consumer typically has 3 – 4 streaming subscriptions. With increased competition, it is likely that Netflix has experienced higher churn (users leaving its service). This is especially true of its most profitable and mature market – US and Canada – where viewers have the most options.

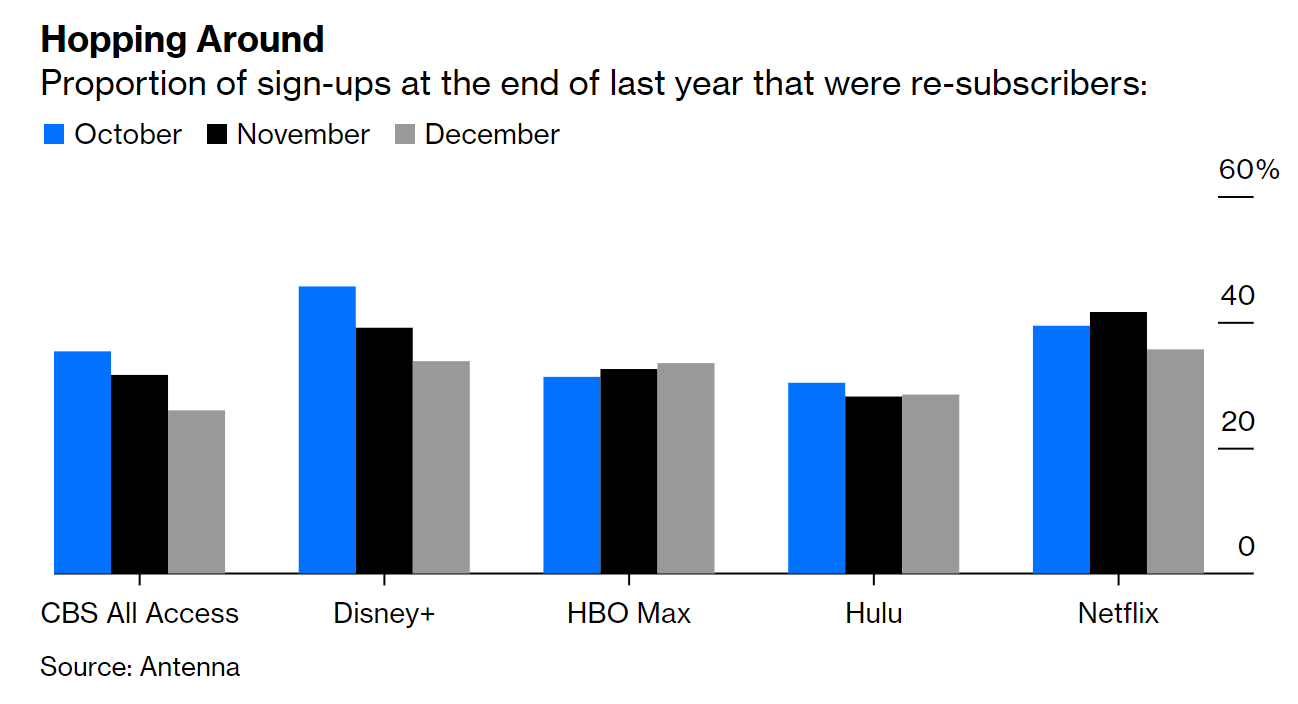

In fact, according to Bloomberg, for Q4 2020, ~40% of new subscribers of the various streaming services are people who have subscribed in the past. This means, as the streaming market becomes more mature, customer loyalty decreases. Viewers will pause subscriptions and will continue only when a show they want to watch appears. This makes the business even more hit-driven than before.

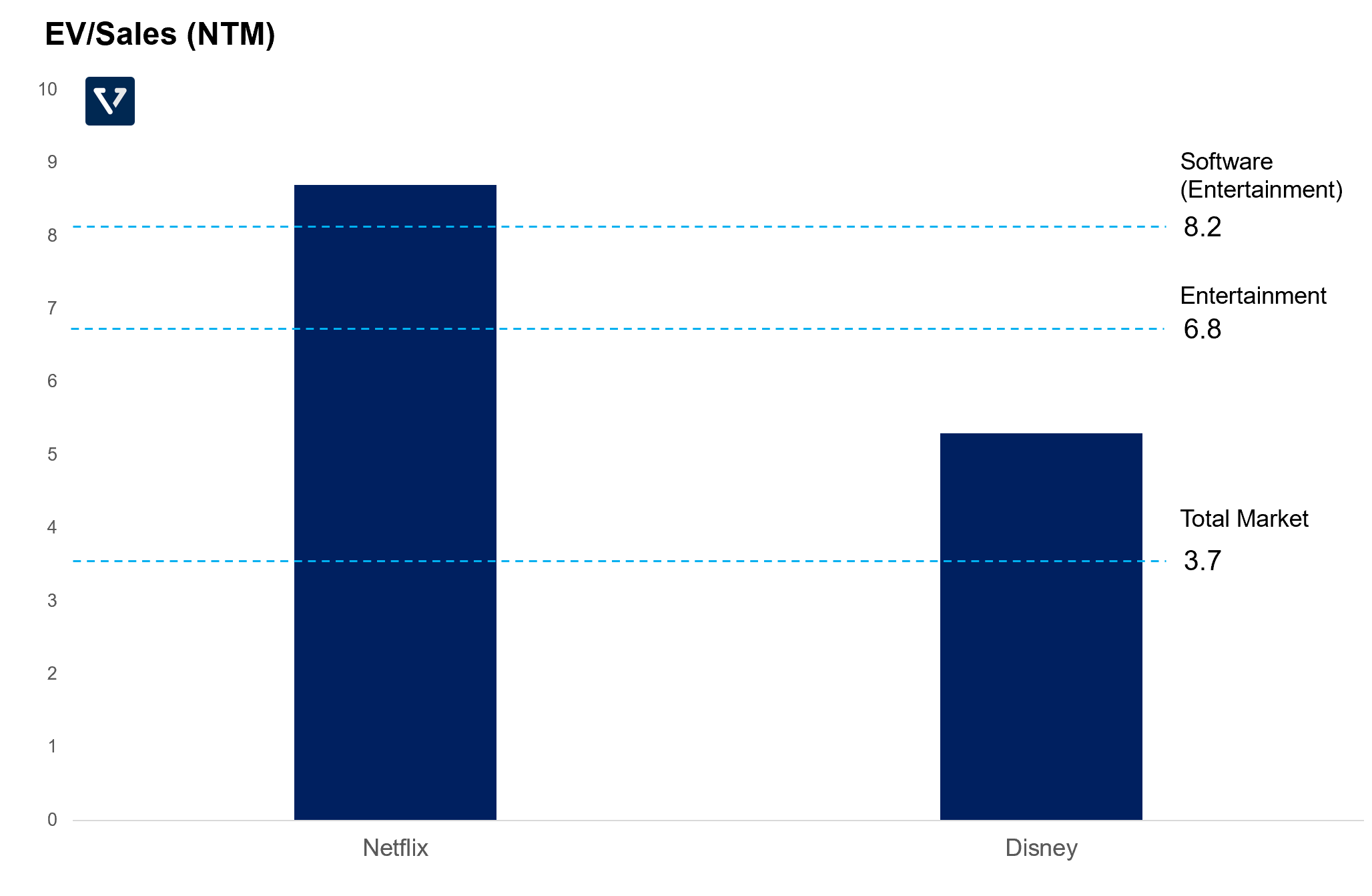

Valuation concerns

Currently, both companies are valued highly by investors, depending on the lens you look through. If you compare to the overall market, the Enterprise Value/Sales (EV/S) ratios for both companies are above the market by more than 2X. But, compared to the entertainment or the software (entertainment) industries, they are more reasonable.