Skip to content

Skip to content

This week, we discuss the increasing trend of companies “having their cake and eating it tooâ€: Amazon and Palantir.

Having your cake and eating it too

As the saying goes, you can’t have your cake and eat it too – but what if you can?

Warrants

When one company establishes an economic relationship with another (be it through a partnership agreement or M&A), both parties typically share in some upside. But when contemplating these deals, these companies often consider the market reaction to the proposed transaction. For example, in an M&A transaction, if the market reacts positively, a pop in the acquirer’s market cap can help cover the economic cost of the acquisition. We saw this with NVIDIA’s proposed acquisition of ARM and Square’s recent deal to acquire Afterpay.

But in recent years, there have been more companies taking advantage of the market’s reaction to get even more economic benefits. When a transaction between two companies is made public, it is often the case that the market cap of the smaller company pops. Knowing this, the larger company can pre-empt the market’s reaction and purchase shares of the smaller company. Here are a few examples:

Amazon is one of the most feared/admired companies publicly traded today. When Amazon announces new products or acquisitions, the share prices of its incumbents typically fall, and conversely, when it announces new partnerships, the share prices of its partners can pop.

In order to take advantage of this phenomenon, the company has been requesting warrants in companies it does deals with. These warrants are agreements for Amazon to buy the vendors’ stock in the future at below market prices. In his excellent book, Amazon Unbound, Brad Stone wrote about one such example. In the spring of 2016, Amazon leased forty Boeing 767 freighters, to be rebranded as Amazon Prime Air, from two midwest regional airlines (ATSG and Atlas Air). As part of the deal, Amazon purchased warrants for the two airlines. In the month after the announcement of the deals broke, the share prices of the airlines went up 49% (for ATSG) and 14% (for Atlas Air). After all was said and done, Amazon not only secured expansion capacity for Amazon Prime Air, but also earned almost half a billion dollars in return on its investments. Talk about having your cake and eating it too.

“Fantastic Job – this is how it’s done!†– Jeff Bezos emailed when he heard the news.

Other companies have been following in Amazon’s footsteps. When Shopify signed an exclusive deal with Affirm (read more about Affirm), Affirm granted Shopify a 5% stake (or 20.3 million shares) via 10 year warrants (at the time of the IPO, worth more than $2 billion). The share price of Affirm has declined 30% since then, but after news broke last week that Amazon too will be using Affirm as its buy-now-pay-later solution, Affirm’s share price jumped more than 40%. I suppose, for Shopify, it’s a nice consolation price considering that its exclusive buy-now-pay-later provider is signing with its chief competitors.

I’ll invest in you, and in return, you buy my products

Another way to have your cake and eat it too, is for one company to invest in another and in return ask for the other company to buy their products. Palantir has been making news for employing this strategy on SPACs. As of July 2021, the company has invested in more than 10 SPACs, and gets multi-year contracts in return. Palantir said that in most cases, the long term value of the contracts it signs with the investee exceeds Palantir’s upfront investment. In other words, by leveraging its balance sheet (the company has invested more than $300 million of cash in SPACs, or ~10% of its cash on hand), Palantir is acquiring revenue, while having the opportunity to participate in the equity upside if the investments appreciate.

Palantir’s expanding margin

What if the reason Palantir is investing in these SPACs is not only to expand revenue, but also to learn?

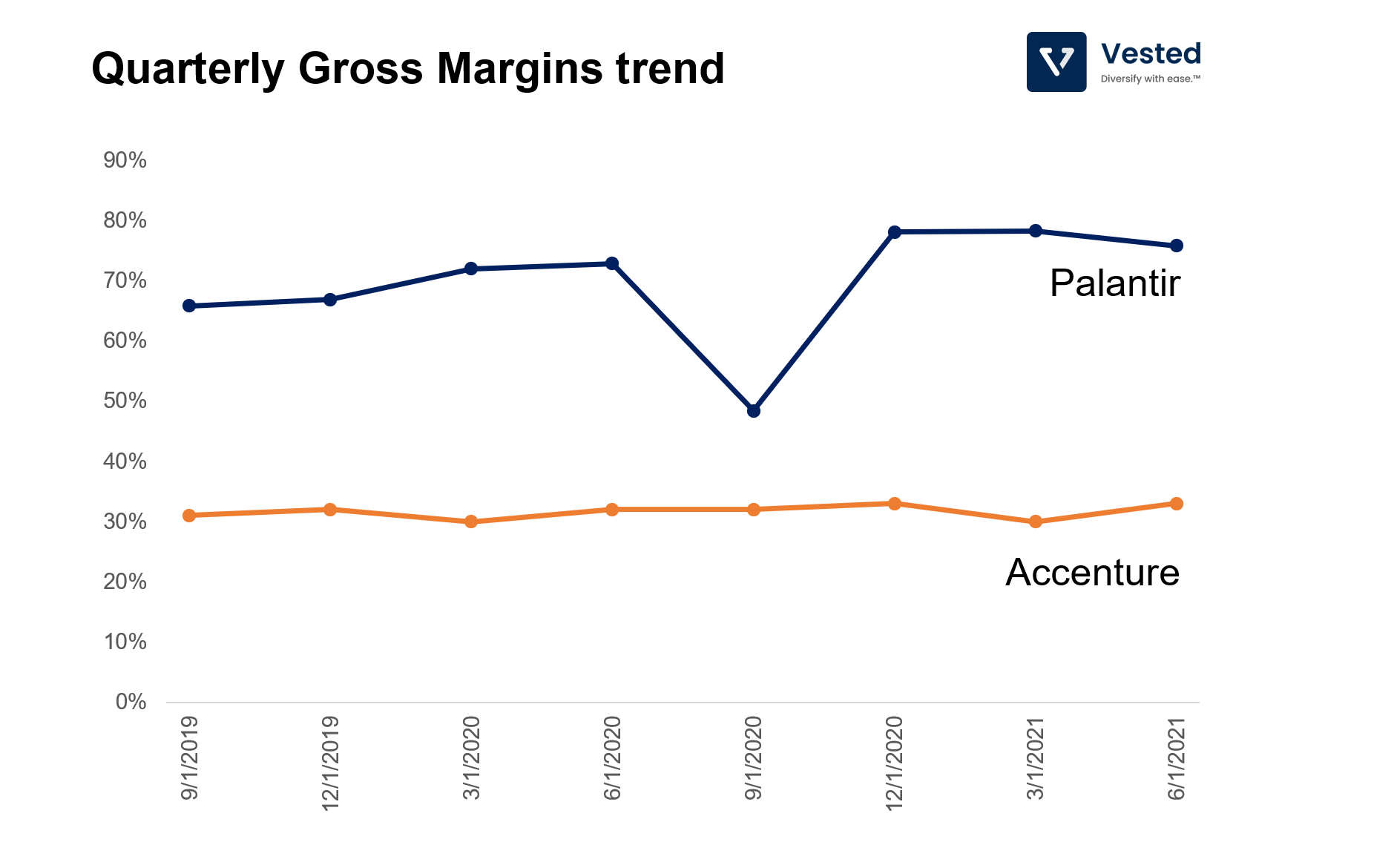

When the company first went public, one criticism that it often received was that it was not a SaaS company, but rather a glorified tech consulting firm (more akin to IBM or Accenture than a SaaS provider). But it appears that Palantir is doing something different, and you can see this from its gross margin trends (see Figure 1).

Technology consulting is typically a low gross margin business. Accenture averaged 32% gross margin in the past 4 quarters, while IBM’s services averaged at about 34%. In contrast, Palantir went public at a gross margin of 66% (Q3 2019) and has increased its margins to 76% (a 15% increase).

Palantir is a data analytics company. It sells to governments (the military, the CDC, the HHS, etc.), banks, biotech companies, utilities, and other hard to sell into entities. Because these customers have their own unique needs and data sets, Palantir has to spend significant time integrating its software with the customers’ data early on in the engagement process. At this early sales stage, Palantir exhibits consulting-like characteristics. Because of this long integration process, Palantir categorizes its customers into three cohorts (from their S-1):

- Acquire phase: Customers who generate less than $100,000 revenue. In this phase, Palantir runs a short-term pilot of its software at no or low cost to its customers. As such, Palantir operates these accounts at a loss. Ideally, customers from the Acquire phase move on to the Expand phase, but that is not always the case.

- Expand phase: In this phase, Palantir expands into a larger pilot with the customer, typically generating more than $100,000 but still contributing negative margins (in fact, at this phase, the losses are larger than in the Acquire phase).

- Scale phase: In this final stage, the consumer finally becomes self-sufficient in using Palantir software, and therefore requires less support. Palantir defines a customer in the Scale phase as any customer that generates more than $100,000 in revenue in a calendar year, with a positive contribution margin during the year.

Understanding how Palantir thinks about the lifecycle of its sales process is helpful. As you can see, because the integration process can be complex and time consuming, once completed, it is unlikely that the customer will leave (it will be very costly to do so).

In order to make the model work, Palantir deploys a lot of engineers in the field, working with their customers to integrate their data into Palantir’s platform. It’s a way of getting R&D to develop products for customers’ specialized needs.Once Palantir’s platform is mature enough for a specific use case, extending the platform to other customers in the same vertical becomes much easier. Yes – Boeing and AirBus have different proprietary data sets they bring to the platform, but the analytical insights they want out of the platform are relatively similar. You can see this in the company’s earnings deck. Beginning in 2021, Palantir started to show the slide below in its earnings deck. There are two key messages here: (i) battle-tested and (ii) speed of integration.

Perhaps this is the reason why Palantir is investing its cash to invest in SPACs. The SPACs they invest in are companies that operate in therapeutics, ad tech, financial services, EV charging, and geospatial monitoring. So if the experiment works, Palantir can:

- Get the cash investment back as revenue

- Participate in the equity upside of the investment

- And learn to build software for these disparate specialized use cases

The ultimate having your cake and eating it too.