Skip to content

Skip to content

We have a lot to cover this week, as it is earnings season here in the US. In this week’s blog, we cover Apple, Facebook, Amazon, Microsoft, and Google, and extract industry trends from their earnings.

Apple’s strong earnings

Apple reported another blowout quarterly earnings. Revenue was up 36%, to $81.4 billion. The company is on pace to achieve $86 billion of profits for the 12-month period ending in September (which would be a record year for the company, 51% higher than last year’s record, also a record year). A year ago, analysts were predicting a modest 11% growth. Boy, how they were wrong…

Let’s look deeper beyond the top line to see where this outperformance comes from. Three key takeaways:

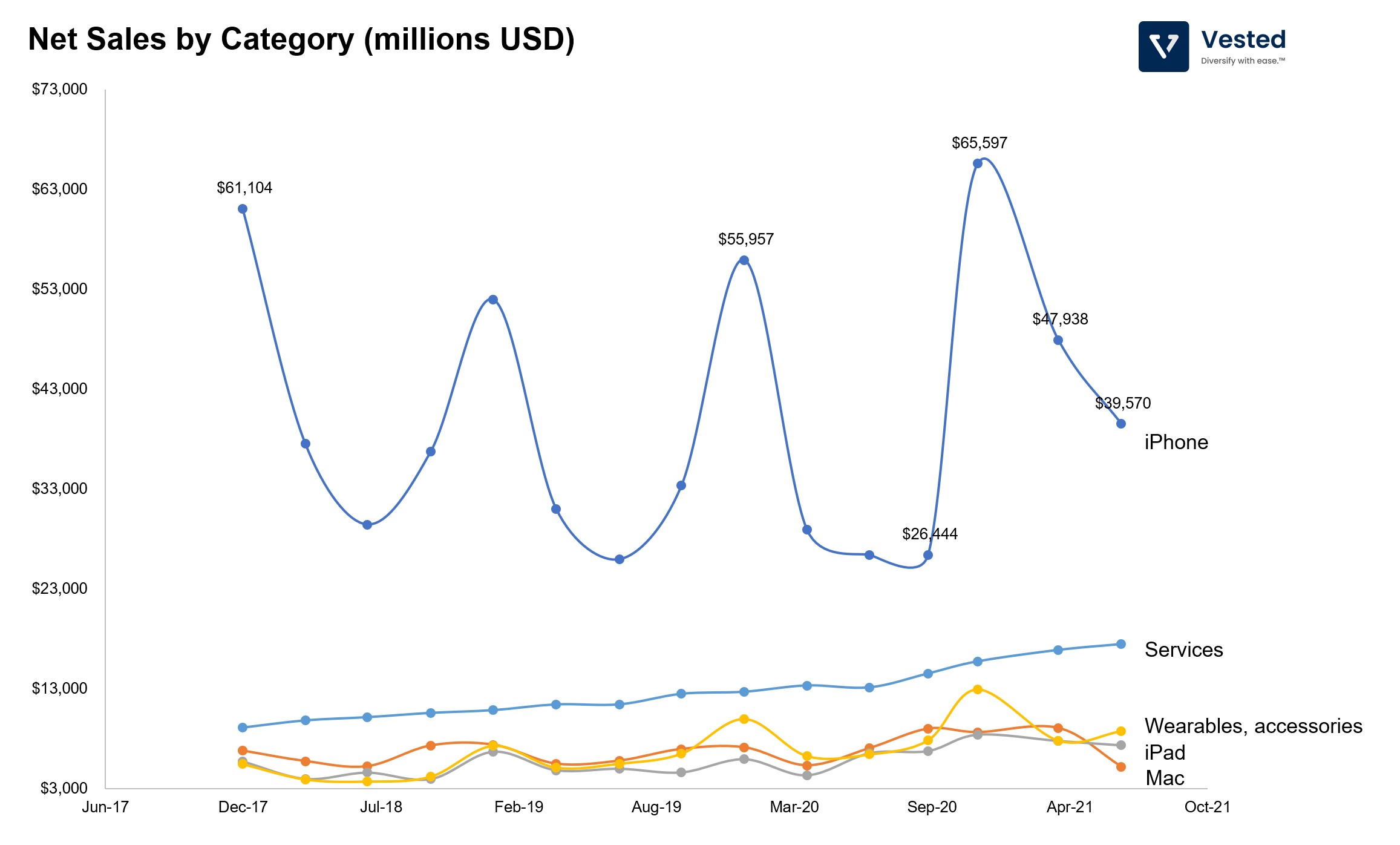

The first takeaway: iPhone sales are really strong. Sales from the past three quarters are the strongest when compared to the past 16 quarters (seasonality adjusted). This is largely because of the launch of iPhone 12, which is a new industrial design (larger, more cameras, 5G, and comes in a Pro version that is even priced even higher).

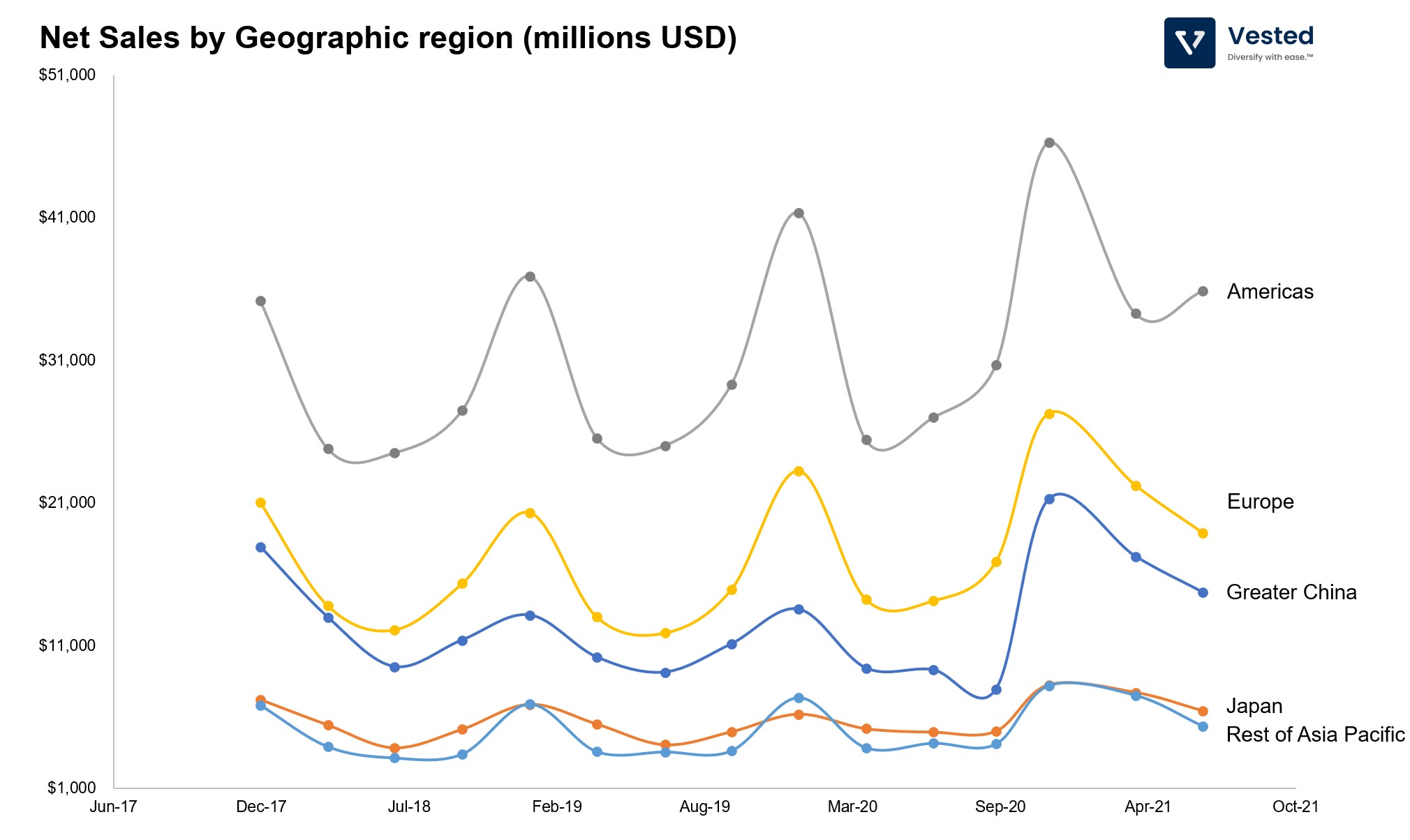

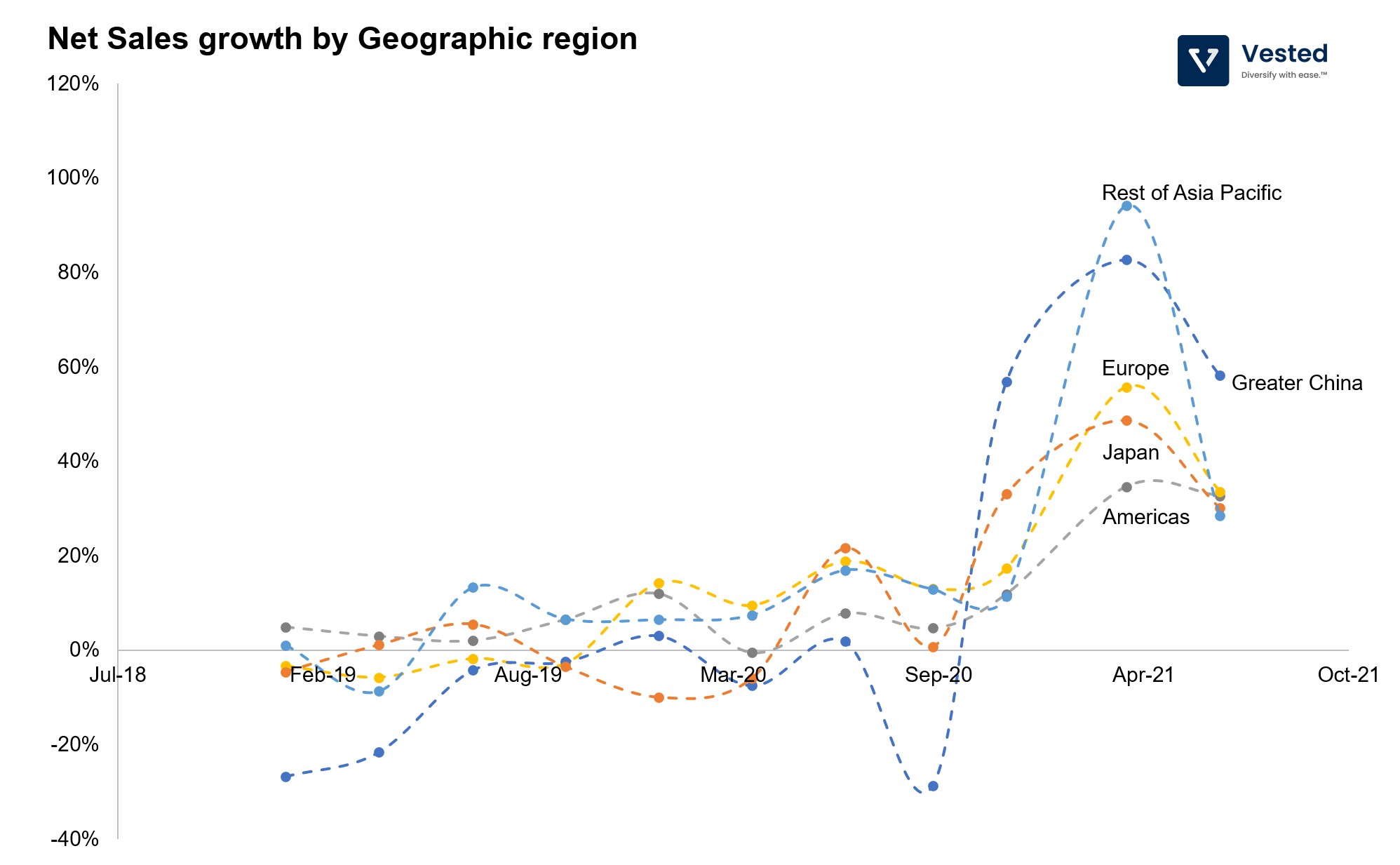

The second takeaway: So, where did the strong iPhone sales come from? Well, the Americas region continued to be the largest contributor to net sales (about 25% – see Figure 2), but what is also important is the rate of change.

Figure 3 below shows the rate of change of net sales by geographic region. Notice that the Greater China region experienced very strong growth rates in the past three quarters. This is because of the new industrial design of the iPhone 12, which prompted more switches and accelerated upgrades. The growth in China also helped with the increased penetration of 5G (China has one of the highest 5G penetration in the world). In Apple’s earnings call, Tim Cook, Apple’s CEO, mentioned that they expect that the transition to 5G will continue to aid the iPhone upgrade cycle.

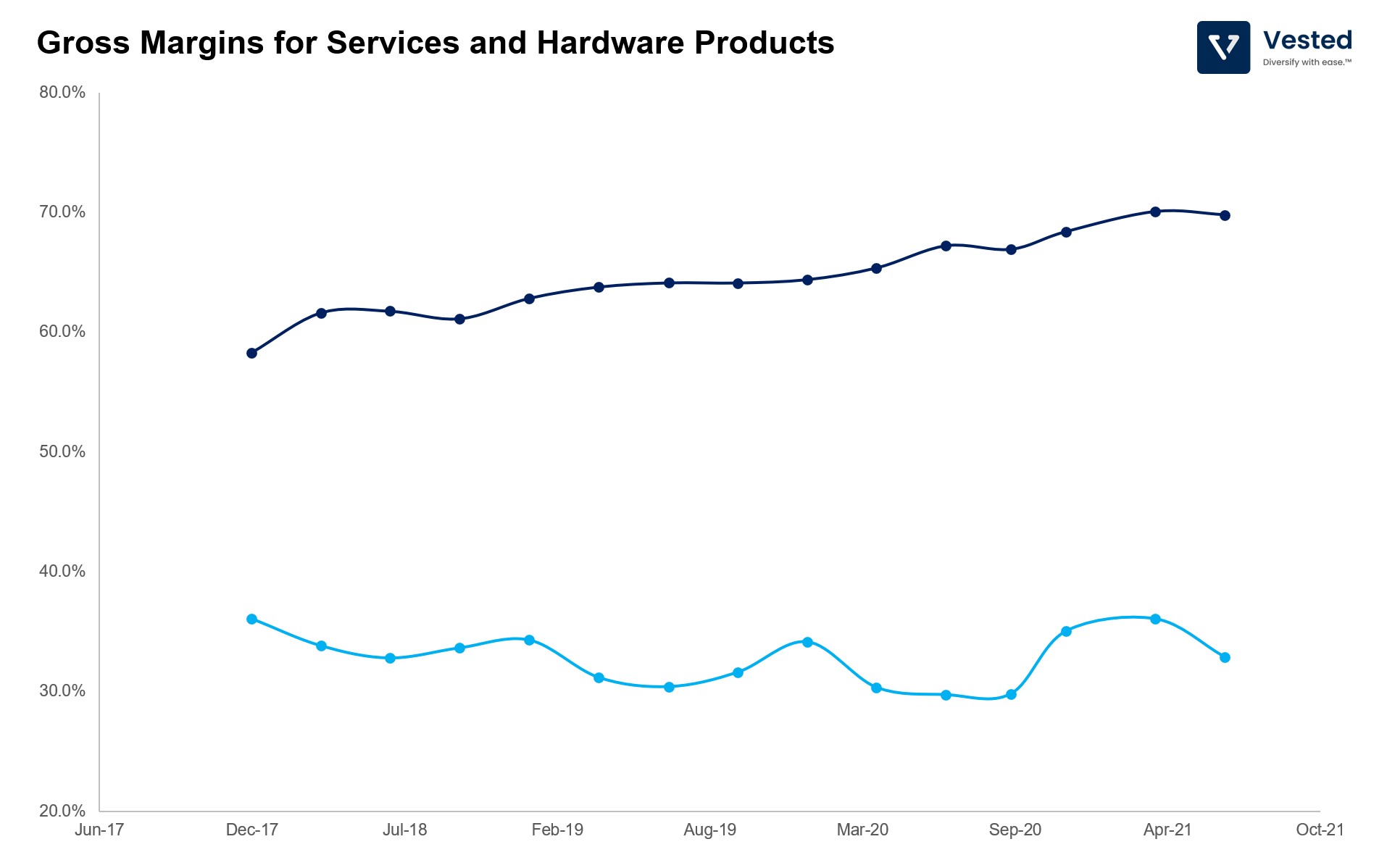

The third takeaway: In Figure 1, you can see net sales from the services segment crossing the $17 billion mark, growing 25% year-over-year. The growth of the services segment is powered by three primary items: ads, app store fees, and Apple care. These are add-on services that allow Apple to increase monetization of its more than 1 billion device install base. The most recent product line that the company is pushing in this segment is advertising.

With iOS14.5 (the new App Tracking Transparency or ATT), Apple knee-capped events tracking for Facebook and other digital advertisers, and at the same time pushed for its own ads platform. The (really) nice thing about the services segment is that it is extremely profitable. In the past quarter, services gross margin hit 70%, up from 64% two years ago.

What’s in store in the near future?

- The company still won’t give accurate sales projections for the remainder of 2021. This is because of uncertainties around COVID and the chip shortage. Apple mentioned in the earnings call that growth in the subsequent quarters will be slower due to chip constraints. If Apple, the largest player in the industry, is feeling chip constraints, expect others to feel it more acutely.

- More share buybacks and dividends. In the past 12 months, Apple has spent more than $83.5 billion in share buybacks and more than $14 billion in dividends – and is still left with more than $90.9 billion in cash (and cash equivalents) on hand.

- The iPhone super cycle may have only just begun. The iPhone 12 achieved a milestone of 100 million phones sold faster than the iPhone 11, and is matching the previous super cycle, the iPhone 6, which accompanied the transition from 3G to 4G back in 2014/2015. With a more than 1 billion iPhone install base, and it still being the very early days of 5G deployment, the iPhone upgrade cycle might have only just begun.

Digital advertising is hot – a boon for Google, Facebook, and Amazon

Most of the largest digital advertising platforms reported strong revenue growth. Twitter, Snap, Google, Amazon’s advertising, and Facebook, all reported strong earnings growth. These companies are enjoying a red hot US ad market, where ad spending is on track to be the fastest in the post WW2 era.

Let’s focus on the top three ad platforms: Google, Facebook, and Amazon’s advertising business. Generally, there are two types of digital advertising:

- Brand advertising: You spend money so that consumers may remember to buy from you on a later date. For example: Volkswagen showcases its new electric Golf now, in hopes that you will consider the car when you decide to buy an EV in the future.

- Direct advertising: You spend money so that the consumer buys something from you now. For example: You are shown an advertisement for a headphone while searching for the best noise-cancelling headphones.

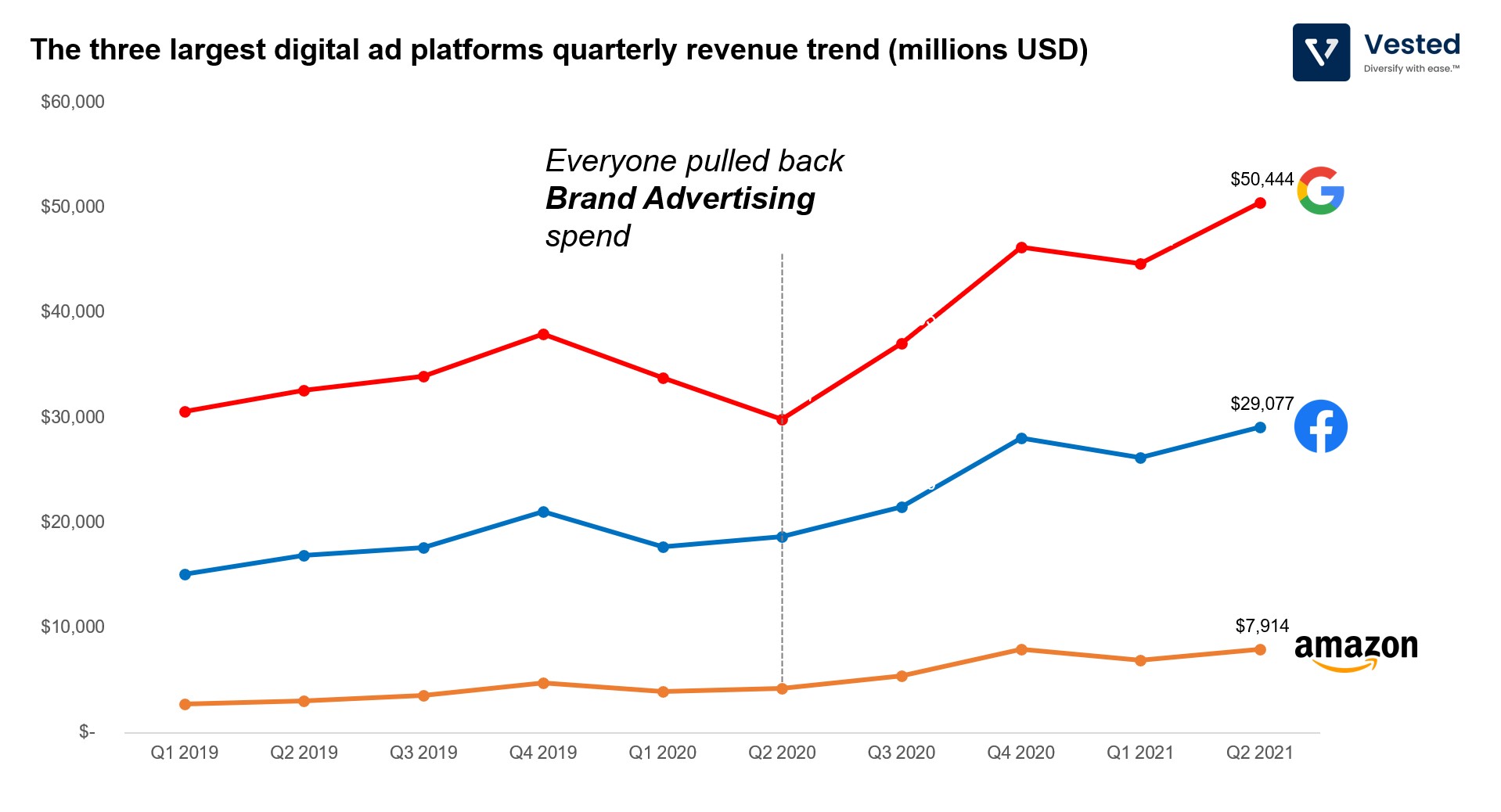

Direct advertising drives the advertisers’ revenue now, while brand advertising may drive revenue in the future. So, when the macroeconomic outlook was highly uncertain (as was the case in Q1 and Q2 2020, when the world went into lockdown), brand advertisement largely stopped. A large element of direct ads from travel also ceased. The company that relies the most on these two categories is Google. This is why Google’s revenue in Q1 and Q2 2020 went down the most. Now that the world is reopening, spending on both direct and brand advertising re-accelerated, and as a result, you see Google’s revenue growing rapidly again (red line in Figure 5). The company is making almost double what it was making three years ago.

In contrast, Facebook’s business is largely predicated on direct ads. For Facebook, these direct ads are largely placed by small businesses, games, apps, and ecommerce. Facebook’s ad platform works on an auction system. Therefore, any softness in brand advertising in Q2 is filled up by direct ads spend. This is why, unlike Google, Facebook did not see much of a decline in Q2 2020. But this is also why the App Tracking Transparency (ATT) feature that Apple rolled out earlier this year will likely impact Facebook the most. For direct advertising to work well, you have to measure the conversion event, so that you can determine return on investment of ad spend. Apple’s new ATT allows users to easily opt out from being tracked (while favoring Apple’s internal ads platform). This will hurt Facebook the most.

Because of ATT, Facebook near term growth may be negatively affected. To counter this, the company is investing heavily down the conversion funnel. Here is what Mark Zuckerberg said in Facebook’s earnings call (emphasis ours):

“But I think overall, the strategy is really to work our way down the funnel from discovery and all the things that we’re already world-class at with ads to making it so that those ads increasingly point to Shops across our different services.

In order to do that, each layer of the funnel that we’re working on, we want to be world class on its own, which means that basically, there’s this whole long tail of functionality that businesses have come to expect on the web and from other tools, and we need to make sure that that’s available for Shops and business messaging and all the tools, whether we do that through partnerships with other e-commerce companies or building it up ourselves.

So it’s — we’re seeing meaningful improvements every quarter in this in terms of how effective these are. There are already a pretty meaningful number of merchants and people who are using Shops, and we expect this to compound over the coming years.â€

The goal of advertising is to help advertisers get customers that can be converted into sales. If tracking is broken outside of Facebook platforms, the natural counter is to internalize the conversion, by bringing commerce into Facebook platforms (done through partnerships with Shopify, through WhatsApp, and other Facebook platforms).

As for Amazon, the company’s ad platform mostly caters to direct ads (the ads are promoted placement – they show up when you search for things). And because Amazon internalizes the conversion events (you see the ad, click the ad, and complete the purchase within Amazon), the company is not impacted by ATT.

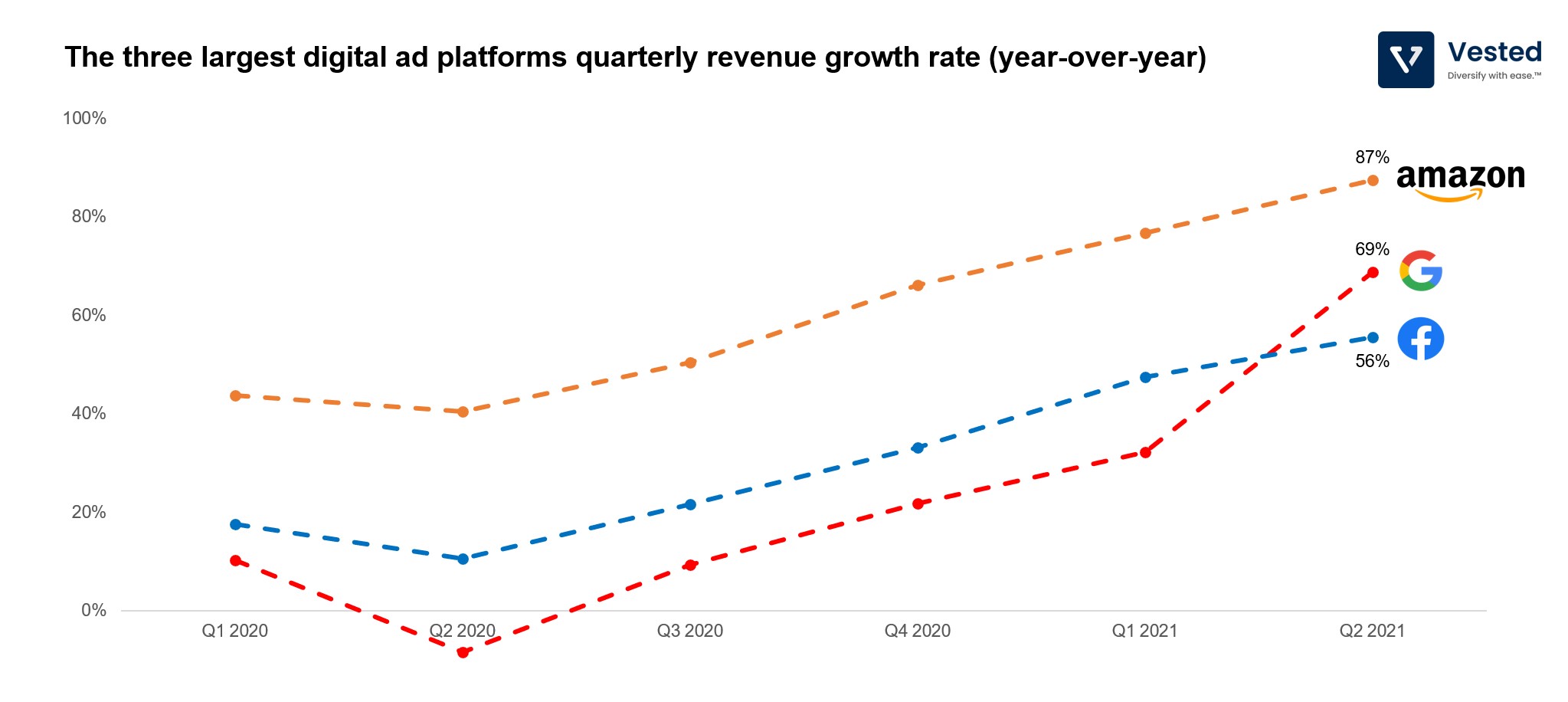

Figure 6 below shows the year-over-year growth rates of Amazon’s other segment (mostly ads) and the quarterly ads revenue for Google and Facebook. Even though Amazon is the smallest, it continues to grow the fastest.

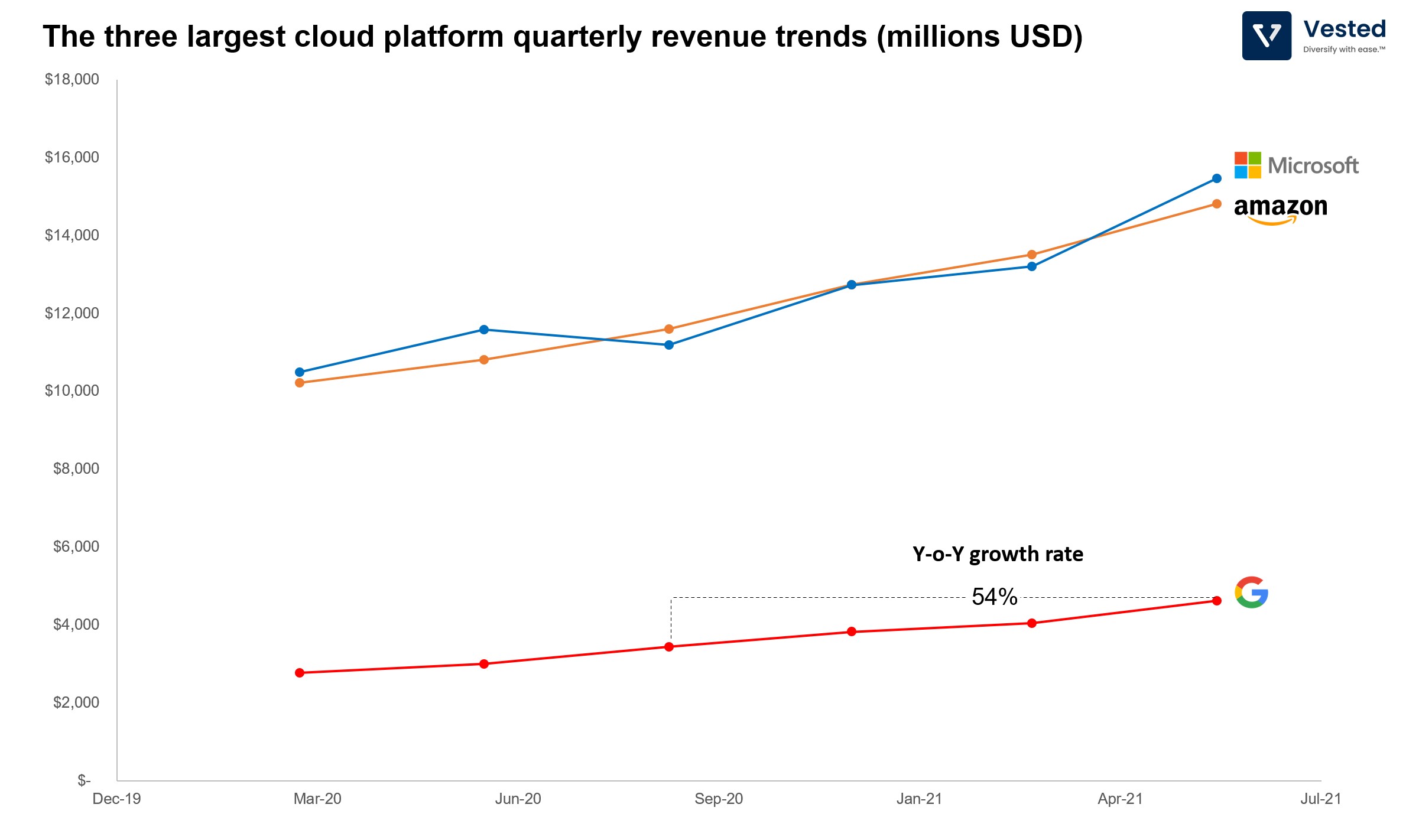

Cloud Computing growth continues: Amazon, Microsoft, and Google

Ok, let’s shift gears and talk about cloud computing macro trends. Second only to ecommerce, the shift to cloud computing is one of the largest beneficiaries of the work-from-home and global lockdown from the past 15 months. Gartner expects that the global spend on public cloud will grow another 23% in 2021, up to $332 billion. In this market, the three largest US providers are Amazon, Microsoft, and Google. Amazon, via AWS, has the largest market share (estimated to be 32%), while Microsoft is at 19% and Google at 7%.

Figure 7 shows the revenue growth for all three companies. Here are three key takeaways:

- Despite the smaller market share, Microsoft’s Server products and cloud services segment generates about the same amount of revenue as Amazon’s AWS.

- Both Microsoft and Google bundle other cloud and productivity services into this revenue segment, and do not break it out cleanly, unlike AWS. So this is not quite an apples to apples comparison.

- Google’s quarterly cloud revenue exceeded $7 billion, a 54% growth from a year ago.

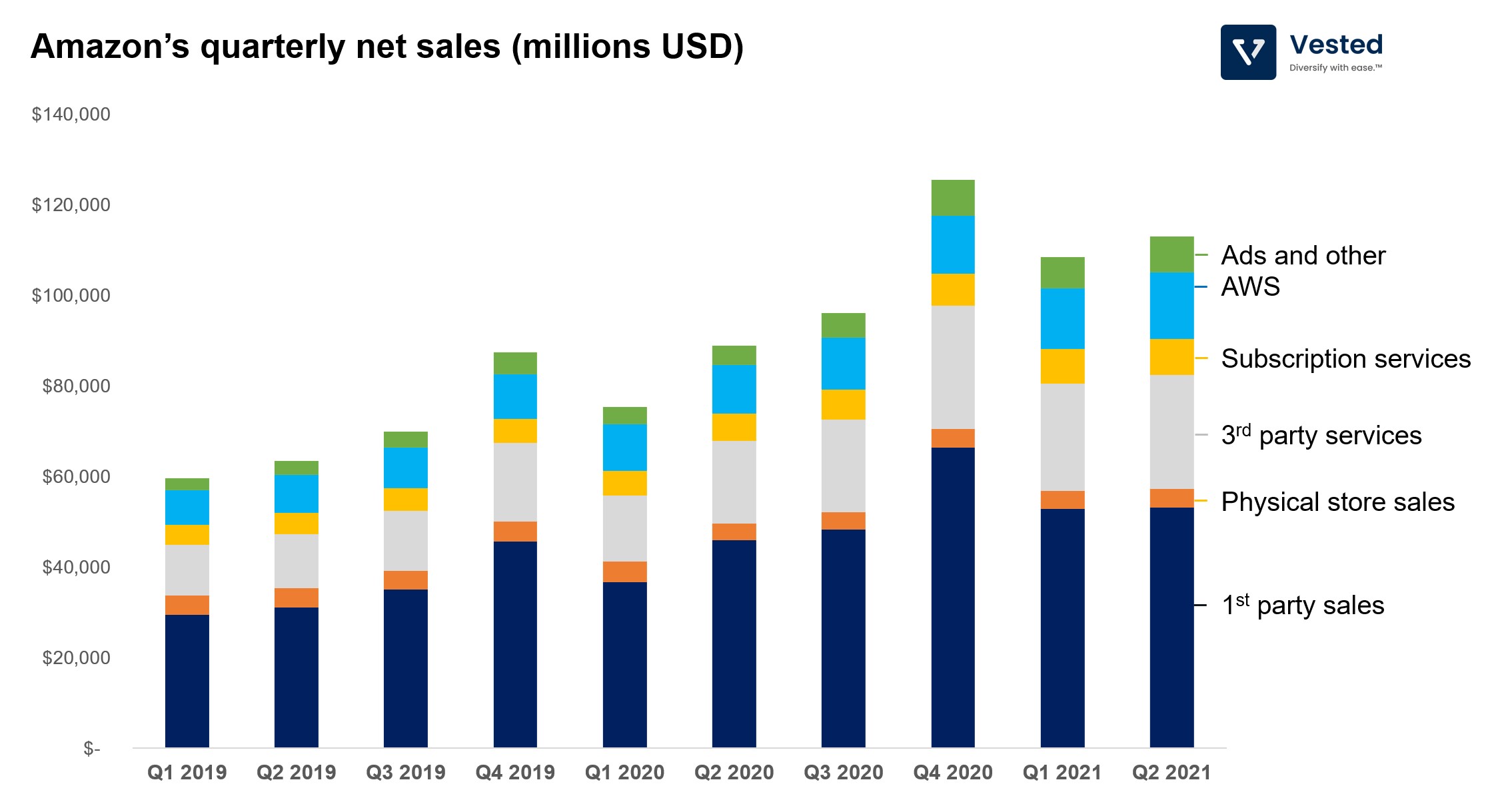

Ecommerce Slowing Down: Amazon

Last but not least, the ecommerce giant, Amazon. The company beat expectations on profits, but reported lower revenues than analysts expected. Amazon reported sales of $113.1 billion (about 2% less than predicted by analysts), with a profit of $7.8 billion (or 23% outperformance on a per share basis). The company also shared a Q3 forecast range that was slightly below expectations. As a result, its shares went down 7.6% after the earnings release.

A big part of the lower forecast is because of reopening in the US. Ecommerce sales were supercharged in the past 4 to 5 quarters, and are now returning to some semblance of normalcy. If you compare Q2 2021 revenues with Q2 of last year, the revenue growth rates look like it’s slowing down – but this is because Q2 of last year was exceedingly strong, making it a bad comparison. However, if you compare the revenue from Q2 2019, Amazon has doubled (!) its top line revenue in 2 years. This is no easy feat considering its size (Figure 8).