Skip to content

Skip to content

Today, we talk about a good old brick and mortar business, Costco, and the decline in valuations happening in the software-as-a-service (SaaS) vertical.

Costco (the big box store that everyone loves)

At Vested, we discuss a lot of tech companies, but today, we are shifting gears and diving into a traditional brick and mortar company.

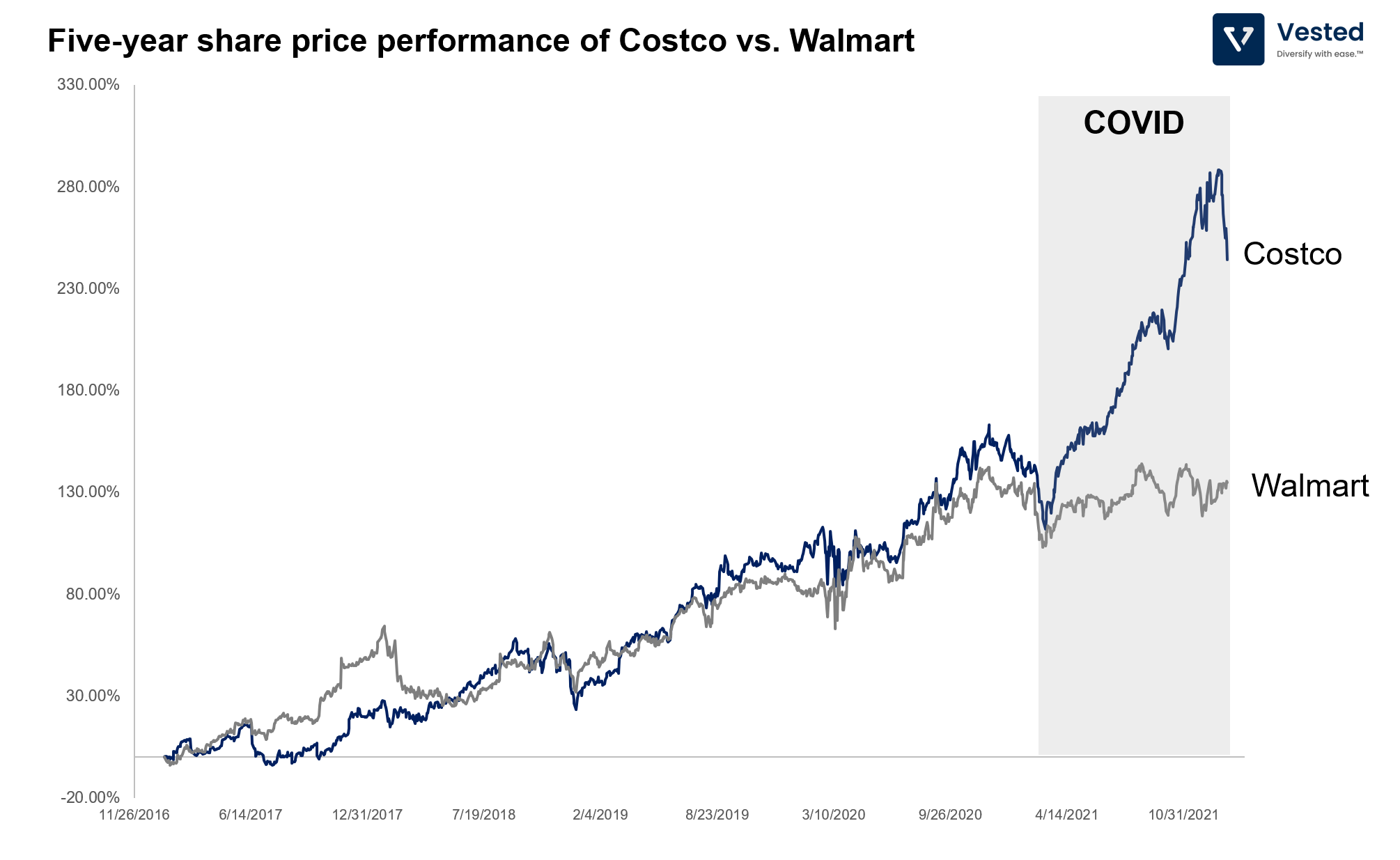

Costco is a giant retail company. It is the 23rd largest company in the S&P 500, with a market capitalization of $223 billion. Although much smaller than Walmart (which has a market cap in excess of $402 billion), Costco is Walmart’s chief competitor.

The returns of the two companies were relatively similar in the past five years – that is, until COVID disruptions started in Q1 2020. Since then, Costco’s share price has been on a tear, while Walmart’s remained largely flat. Why is this so?

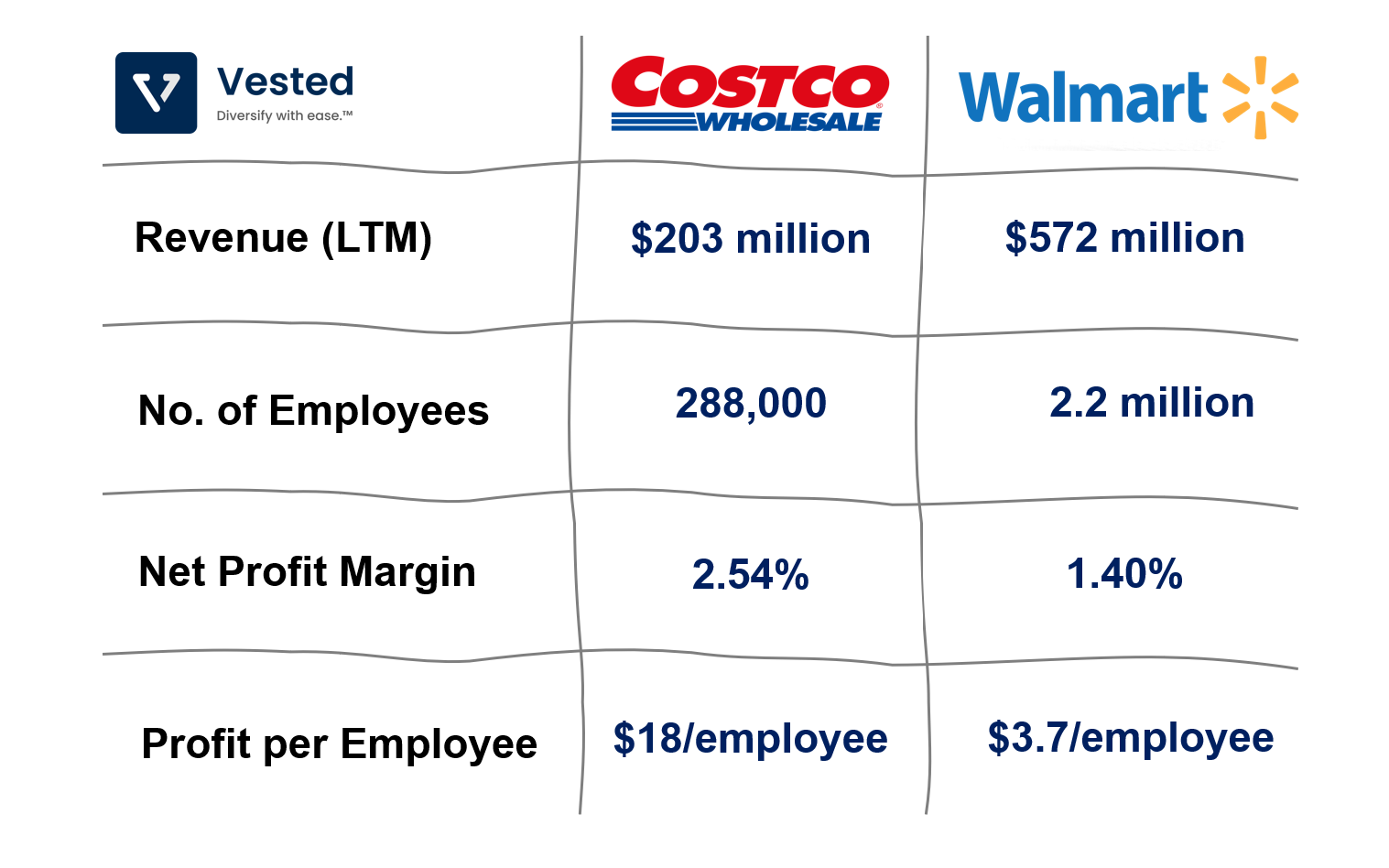

Before we answer that question, let’s look at the top line comparison between the two:

From Figure 2 above, you can see that Walmart is much larger, both by top line revenue (2.8x larger than that of Costco) and by employee base (7.6x larger than that of Costco). Despite the size advantage, Costo is more profitable. Its net profit margin from the last twelve months is 2.54%, higher than Walmart’s 1.40%. As a result, the annual profit per employee for Costco is almost 5x higher than that of Walmart. This suggests that Costco is much more efficient than Walmart.

Costco achieves this by employing several different strategies to its retail operations.

Large warehouses with limited selection

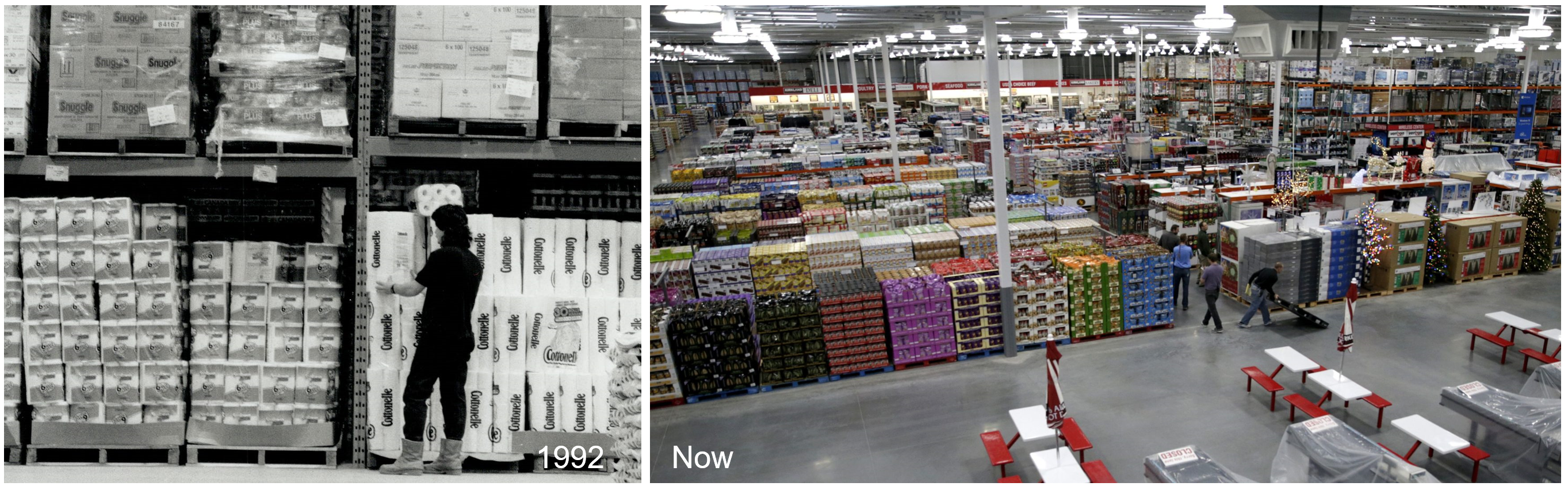

Costco’s stores are not stores. They are warehouses with an average size of 2.5x football fields. Customers come and shop directly on the warehouse floor. This means that Costco can simplify its logistics operations since the space for both storage and display are combined. Here’s an image of a typical warehouse (Figure 3).

As you can see in the above image, over the decades, the warehouse design remains largely the same: Items are sold in bulk and placed on the floor while still on their wooden palettes. This simplifies sorting and shelving items, eliminating unnecessary stocking and sales staff.

Also, notice that Costco has no navigation signs in the warehouse. This is not only a cost savings strategy (you don’t have to update displays as inventory changes), but it is also a sales strategy. No navigation display forces customers to meander around (which inevitably leads to more impulse purchases). They call this treasure hunting. Turns out customers love this.

The warehouse design has a couple other advantages:

- Selling items in bulk means lower theft loss (or shrinkage). Costco’s shrinkage is about 0.12%, much lower than the industry average of 0.5 – 1%.

- Bulk items consume more space, so a typical Costco warehouse only carries ~3,700 SKUs, much smaller than WalMart’s typical 100,000 SKUs. But again, by focusing on a smaller number of items, Costco gains efficiency and is a much larger portion of its vendors’ sales – giving it strong purchasing power.

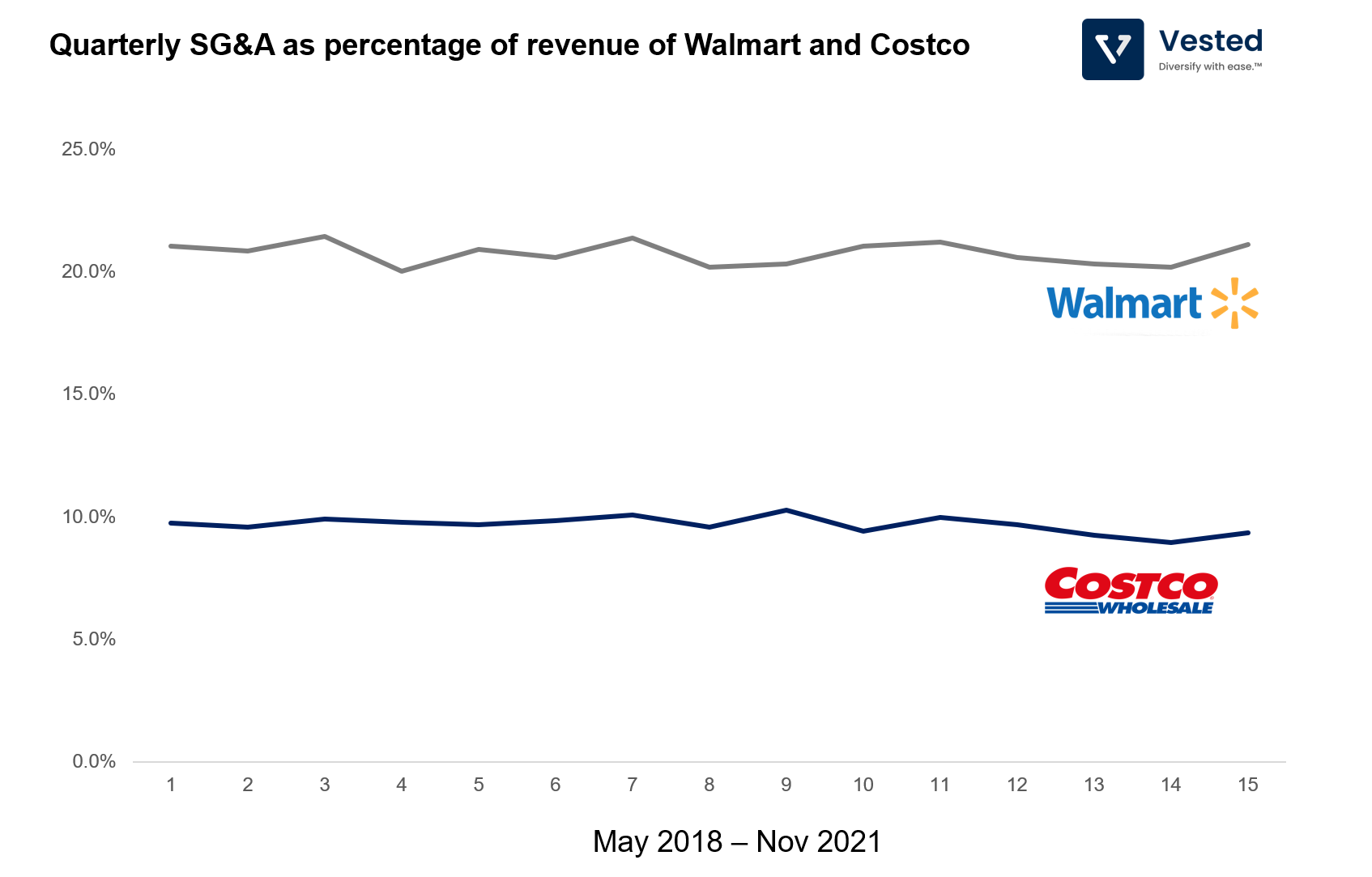

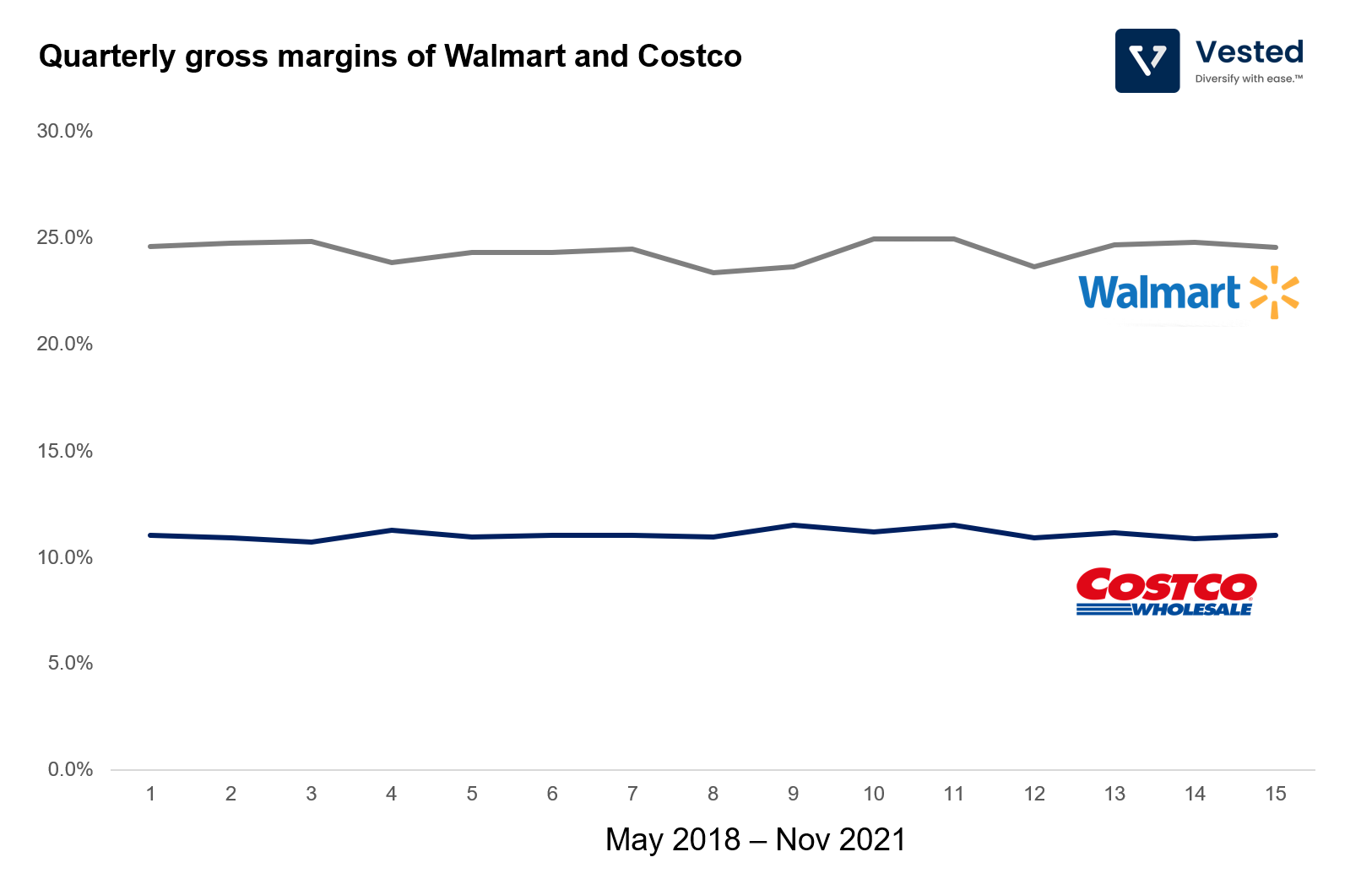

Despite paying more for wages (the company is well known for paying higher than its competitors), which leads to happier employees and lower attrition rates, Costco has lower labor costs, thanks to the efficiencies above. This translates to lower SG&A costs – about half when compared to Walmart (see Figure 4 below).

Low gross margins by design

Costco also employs a strategy where they take lower gross margins on items. The company typically adds about 11% gross margins on items, which is about 2.2x lower than that of Walmart. It can do so because its operations are more efficient. This means that on average, Costco’s items are cheaper.

Members only

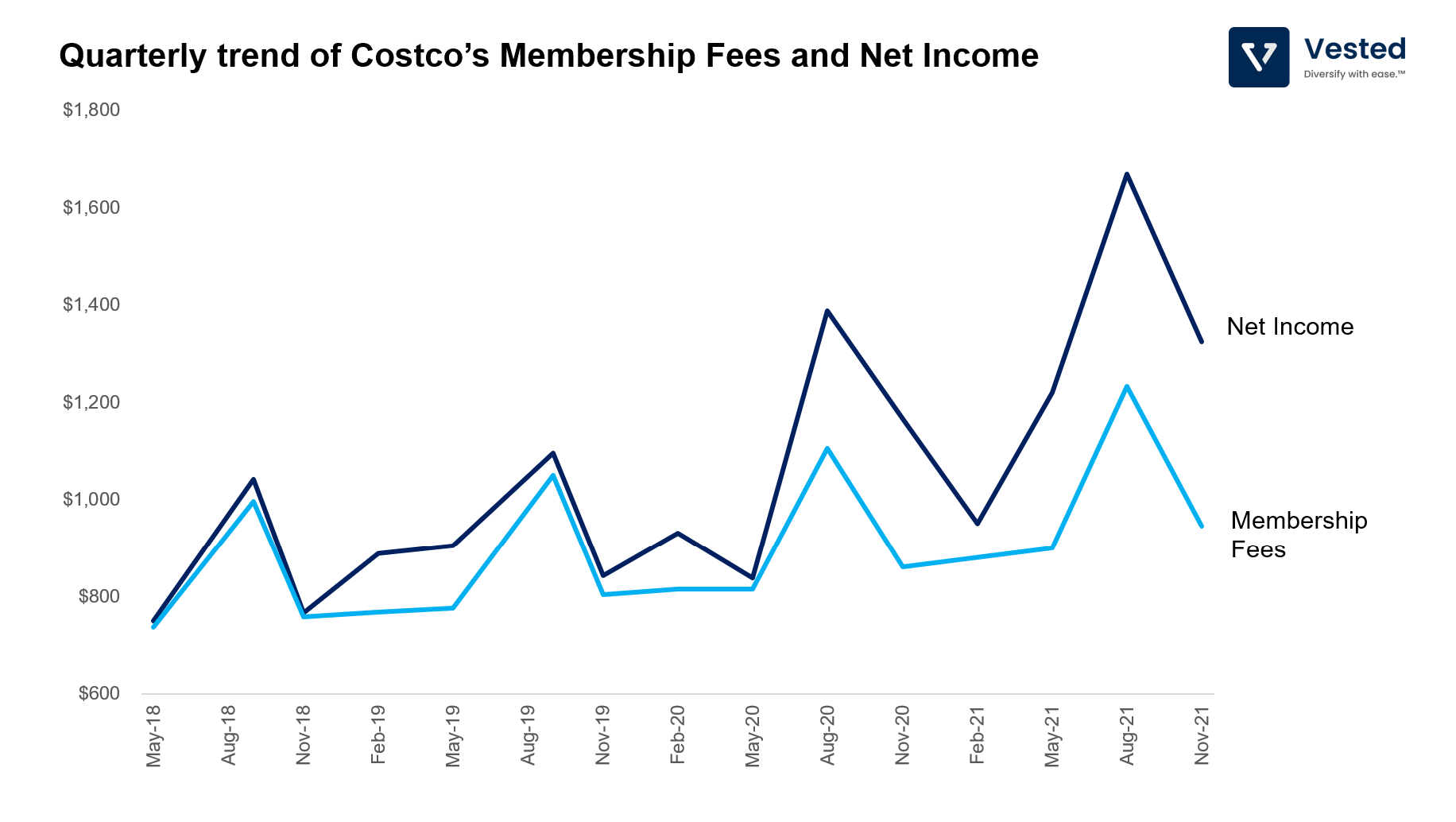

Ok, efficiency alone cannot make a company profitable. To make up for the lower margins on items, Costco charges a membership fee. To shop at Costco and enjoy its best-in-class pricing, you have to be a member. It charges members either $60 or $120 per household per year. Currently, there are 62.5 million households that are its members (renewing at ~90% rate year-over-year).

As you can see Figure 6, this is where the company makes the bulk of its profits (Membership Fees, light blue line, contributes to the bulk of the quarterly Net Income).

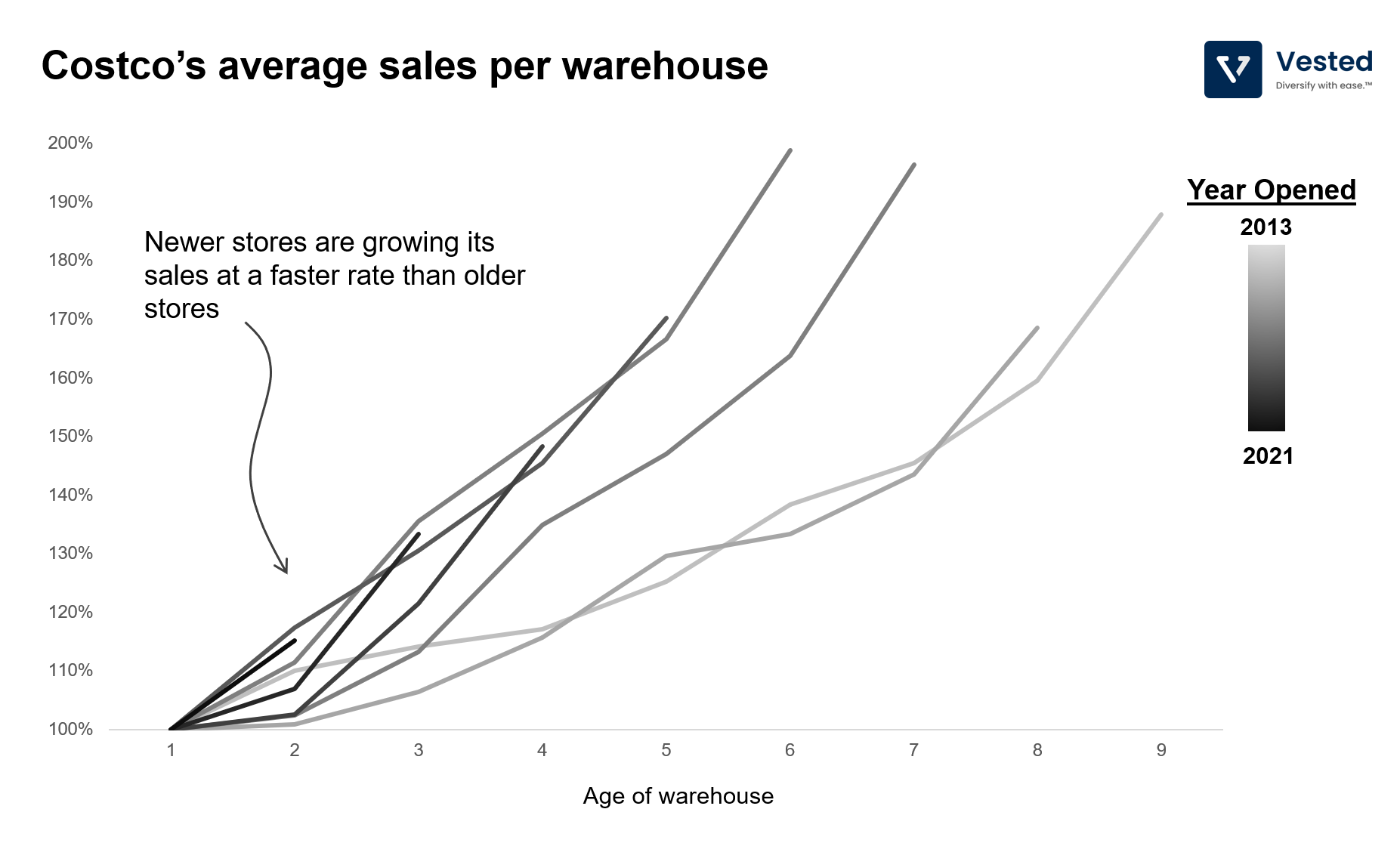

Because you have to be a member to be a customer of Costco, when a new warehouse opens in a new area, it does not have many customers. So profitability and sales are generally lower for newer stores as it takes time for word of mouth to spread. Over time, the new warehouse gains new members from the locality, sales in those stores go up, and so does profitability. But because of the mechanics we discussed above (low costs, good quality, well paid employees), Costco has developed strong customer loyalty, and although it does not spend much on marketing, its same warehouse sales growth is accelerating (see Figure 7).

Ok – enough about Costco. Let’s talk about the valuations of SaaS companies.

Valuation decline in SaaS

In the past weeks, we have been discussing the overall market sell off triggered by the Fed ending its easy money policy and increasing interest rates. The change in Fed’s policy caused a reduction in valuation multiples. So, even without any changes in the fundamentals of the businesses, share prices went down.

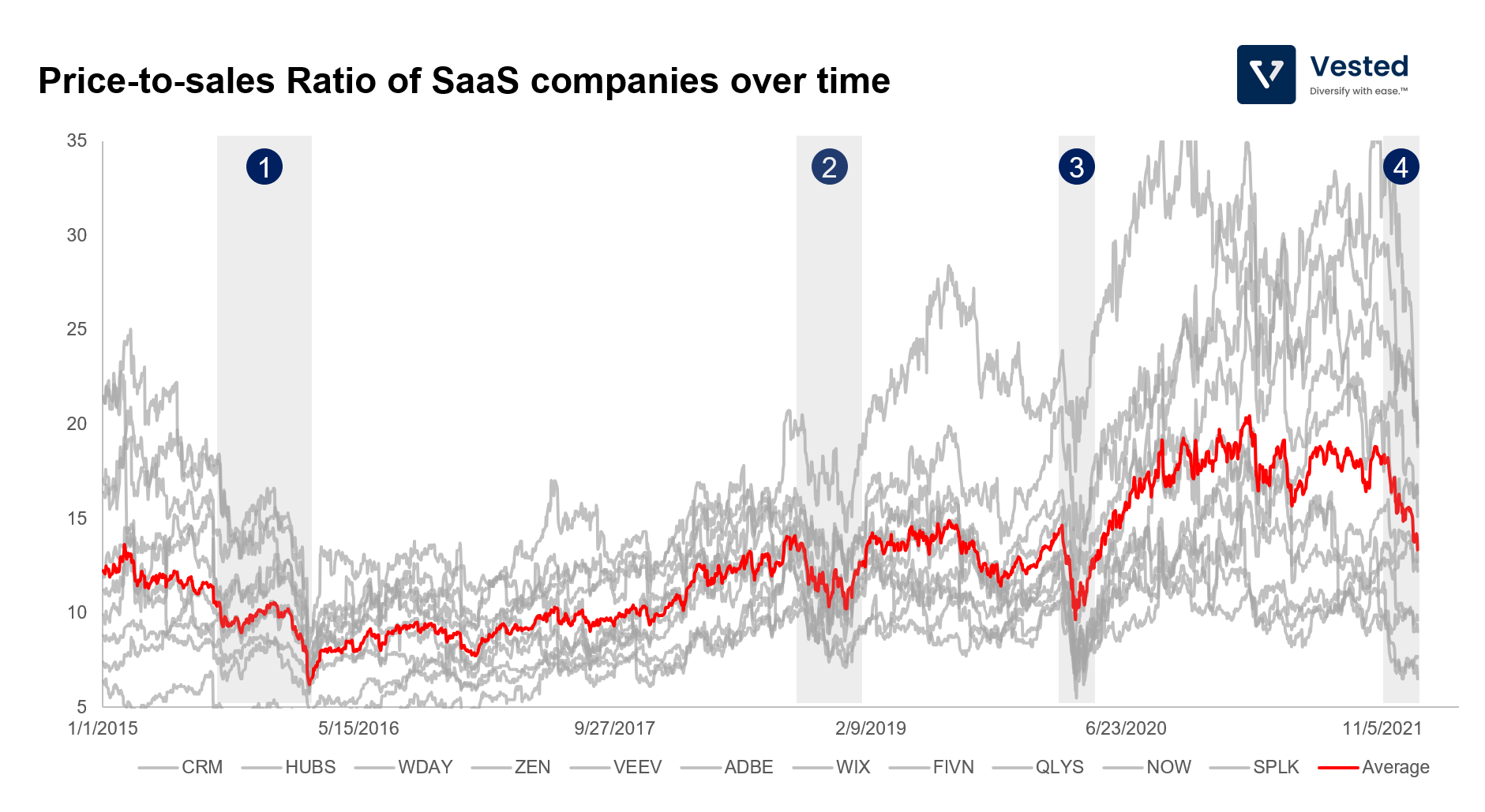

Here, we specifically dissect the valuation changes of SaaS companies. In this exercise, we include 11 SaaS companies that IPO’d before January 2015. We then look at the daily P/S ratio (we use the P/S, or price-to-sales ratio, as a measure of valuation) of these companies from 2015. Figure 8 shows how the P/S changes over time, normalized to the value in January 2015. Grey lines are P/S for individual companies. Red is the average.

In looking back the past seven years, we see four periods where valuations declined:

- (1) In Q3 2015, slump of the Chinese stock market caused US stocks to decline over concerns of global contagion.

- (2) In Q4 2018, US markets broadly, and SaaS companies specifically, went down. Valuation multiples contracted over fears that the Fed would increase interest rates prematurely.

- (3) In February 2020, markets declined rapidly due to the shock of the first COVID global lockdown (can you believe that it’s been two years?)

- (4) Starting around October of 2021, the valuation of these SaaS companies, on average, started to decline. This is because the Fed signaled that it would increase interest rates starting in 2022. Higher interest rates lower the present value of the expected future cash flow, and that means investors will be looking to pay less for a stock. As such, these types of companies tend to experience the most valuation contraction when interest rates go up.

Notice, however, that the average P/S value at the time of writing this article is almost back to January 2015. In thinking about near term outlook, there are three things to consider:

First, how much further will the valuation of SaaS companies decline? Currently, interest rate levels between now and January 2015 are similar. But inflation is currently much higher (7% now, almost 0 seven years ago). To prevent the economy from overheating, the Fed has signalled that it will increase interest rates twice this year.

Second, how long will the decline last? Another difficult question to answer. A large reason why the decline happens is due to high uncertainty. Investors value certainty in macroeconomic conditions. It is not always the case that interest rates increase, translating to lower SaaS valuations. For example, despite interest rates going up from 0.12% in Nov 2015 to 2.40% in March 2019, SaaS valuations also expanded from, on average, 10.5 to 13.5 in the same time period. Once we have clarity on what the Fed will do, valuation multiples of SaaS may expand again.

Third, since increasing inflation forced the Feds to increase interest rates, if we get inflation under control, the Fed may adjust its policy again, right? So the key question is, is inflation here to stay or is it temporarily high due to supply chain issues? (Wow – great question – as if i wrote it myself…) For the better part of 2021, the Feds’ opinion was that inflation was transitory (temporary): As the pricing of products and services are increasing because of global supply chain issues, they will resolve themselves to normalcy.

Turns out, they were wrong. In November 2021, they changed their stance and ditched the transitory label. The increase in inflation was not only due to supply chain issues, but also due to tight labor markets, which in turn drove up wages, which in turn drove up the purchasing power of consumers (US consumers contribute about 70% of the GDP). This type of change is typically longer lasting. Even if the supply chain issues are resolved, wages will not go down (you can’t really reduce people’s wages without layoffs/recession).