Skip to content

Skip to content

It’s been hard to follow the news lately without being bombarded by the latest policy changes or regulatory actions that Beijing is carrying out against various entities. Today, we give you a primer on what has been happening and discuss what might perhaps be the reasoning behind these changes.

China versus Tech

Beijing began its regulatory push back on domestic tech companies in October of last year when it scuttled Ant Financial’s IPO. At the time, the consensus was that the particular intervention was because Jack Ma criticized regulators for being overly-focused on risk and overlooking the credit needs for development.

Since then, Beijing has continued to clamp down its tech industry:

- Beijing waged anti-trust campaigns against its tech giants, fining Alibaba $2.8 billion for anti competitive practices.

- It has asked the tech giants to cease anti-competitive tactics, such as blocking links that lead to other internet platforms.

- Beijing also made the 996 culture illegal (a culture commonly adopted by Chinese tech companies where employees work from 9AM to 9PM, 6 days a week).

- After Didi IPO’d in the US, regulators removed its family of apps from the Chinese App Store.

The clamp down does not stop at regulatory changes. Beijing took equity stake and board seats in its leading tech companies. Last year, regulators took a minority stake and a board seat in Weibo (China’s version of Twitter). This year, they did this to Bytedance (owner of TikTok). And it has been reported that they may do the same to Didi (a report that the company denied, however).

Surely that’s enough intervention, right? Nope.

Tech giants also need to pledge their cash towards Xi JinPing’s common prosperity vision (more on this later). Both Alibaba and Tencent have pledged $15 billion over the next five years (at the time of the announcement, this was 31% of Alibaba’s cash balance). Meanwhile, PinDuoDuo has pledged its next $1.5 billion in profit to rural farmers.

China versus Cryptocurrencies

There are many levels of China prohibiting cryptocurrencies. Over the years, Beijing has instituted various measures to curb the usage of crypto.

- One way to ban cryptocurrencies is to ban the conversion of fiat money to crypto and to ban exchanges from establishing within its borders. In 2013, China did this.

- Another way is to ban value creation on crypto platforms. In 2017, Beijing declared that ICOs were illegal.

- The third way is to ban mining within the country. China has long been a hotbed for crypto mining activities, thanks to the prevalence of cheap electricity. But in June 2021, the mining ban came in earnest, enforced through local electricity companies.

- And finally, if the above fails, ban everything. As we are writing this article, China announced that any crypto (bitcoin, ether and tether) related trading activities are illegal.

This latest ban is different from the ones in the past. Previously, China pushed out crypto exchanges from its borders, but foreign exchanges were still serving Chinese residents. Trading activities via peer-to-peer or over-the-counter were still occurring. This new ban closes this loop-hole and gives state authorities high latitude to monitor and enforce the ban.

China versus Ed-Tech

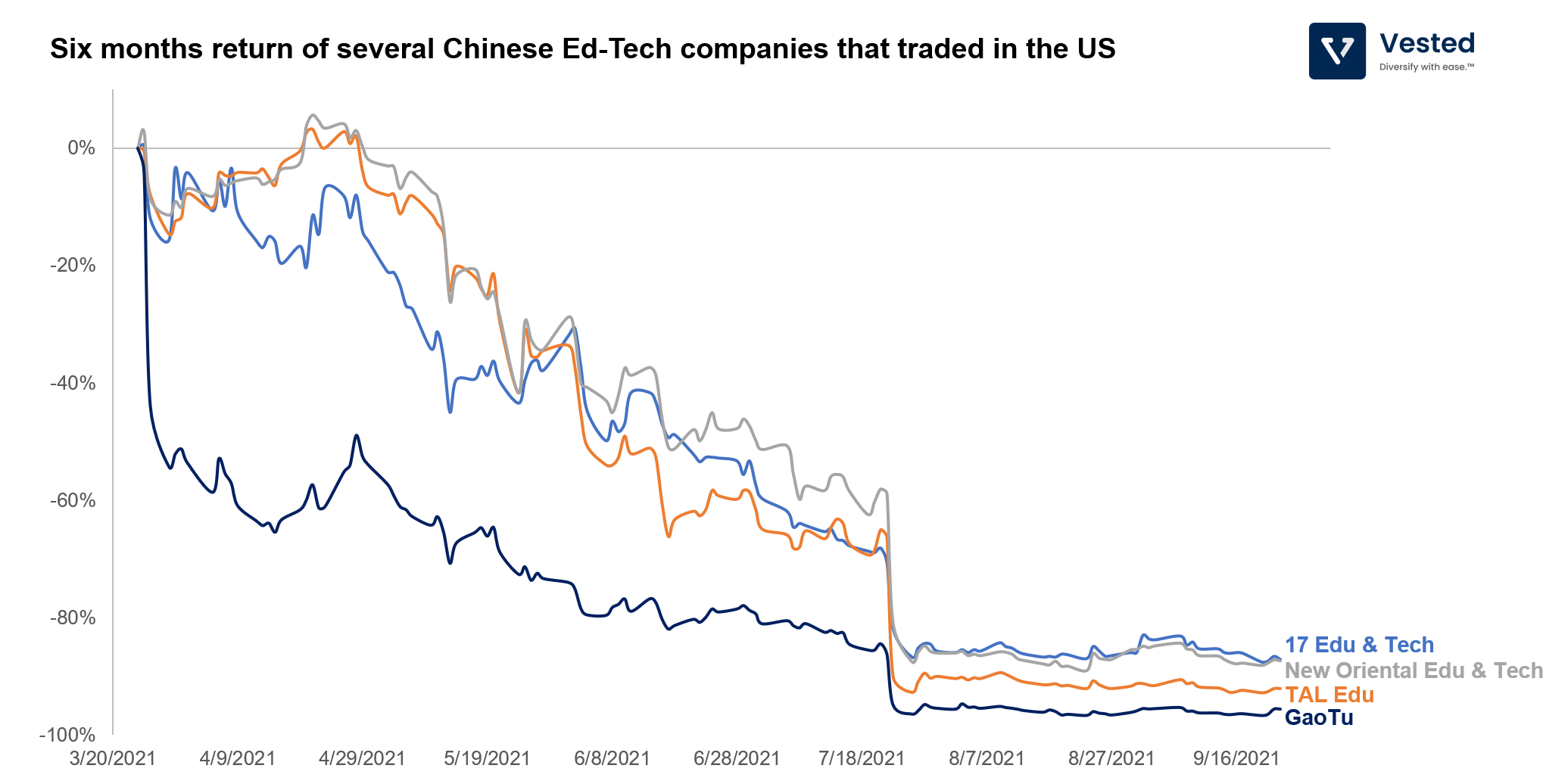

In July 2021, Chinese regulators issued a mandate that existing private tutoring and ed-tech companies become non-profit entities, and that in the future, these tutoring companies would not be not allowed to go public. The news caused a major sell off in the public market (Figure 1).

Private tutoring is a very big business in China, where there are approximately 240 million K-12 students, and where the average family spends on average 11% of their family expenses on education. To calm the market, regulators convened top bankers on a call to explain the reasoning behind the move. Beijing said that the move is a targeted action against a sector that contributes to income inequality (increasingly, only the upper-middle class can afford private tuition) and that Beijing is still supportive of Chinese companies listing abroad.

However, when it comes to China, it’s best to see what they do, rather than listen to what they say…

China versus foreign listings

In July of 2021, the Chinese cyber security regulators announced that companies that have data of more than 1 million users (in China, this means almost all internet based companies) would require a cybersecurity review.

Regulators then took another step. In August 2021, regulators proposed an outright ban on overseas IPO of Chinese firms with sensitive data. The new rules are not finalized and are planned to be implemented in Q4 2021.

The odd thing is that, as we mentioned above, in July 2021, the government stated that they still support foreign listings. But a month later, issued a proposal that seemed to suggest an outright ban of foreign IPOs…

China versus speculation

And finally, the country is also clamping down on speculative culture. On this, the battle is being waged on several fronts:

China versus gambling

This month (September 2021), regulators announced that casino regulations will tighten restrictions on operators, revisit the number of licenses that will be allowed, change the length of the terms, and add governmental supervision, by adding government representatives to supervise companies. About $18 billion in market valuation was wiped after the announcement.

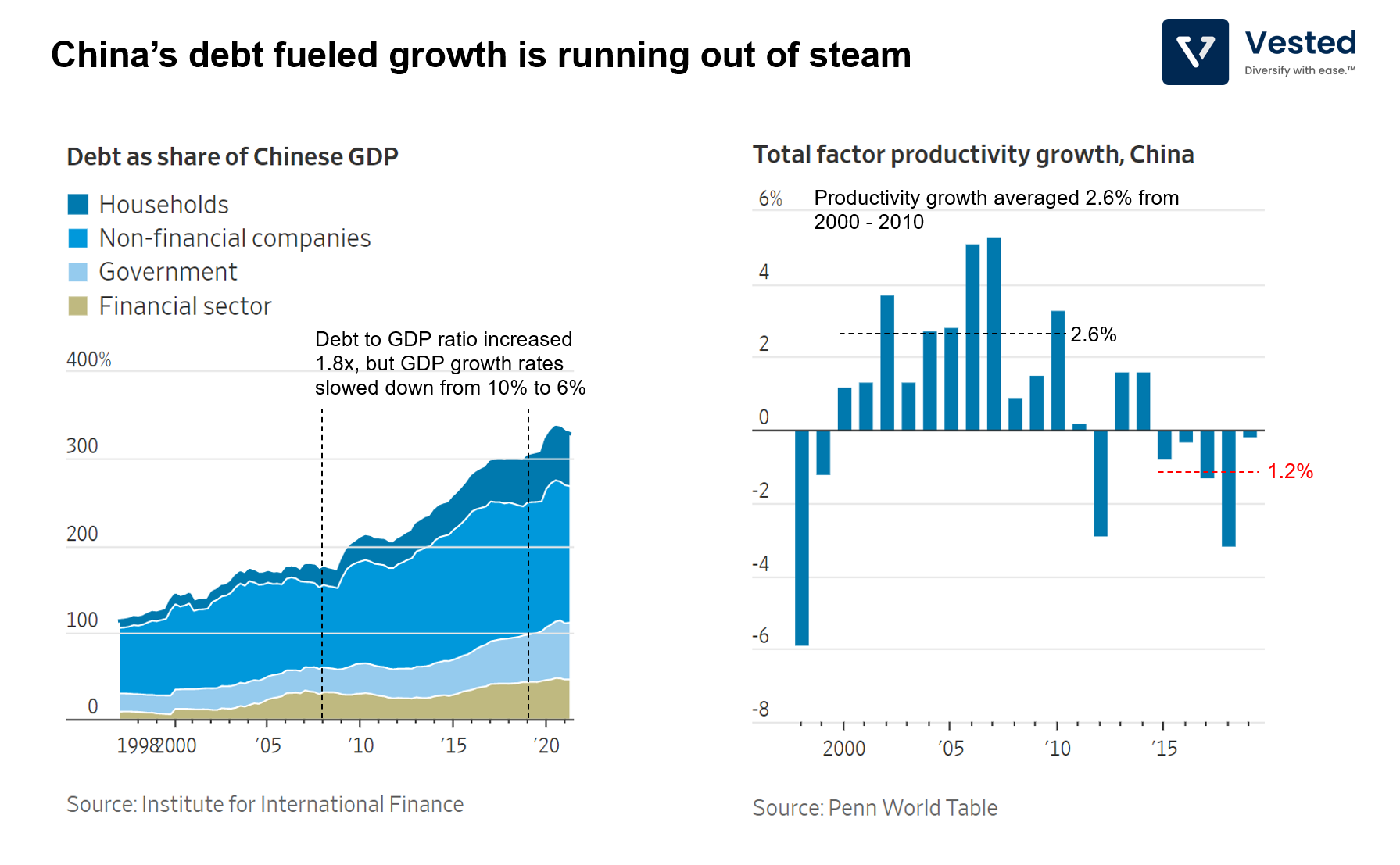

China versus debt fueled growth

The more apt title for this subsection is actually China versus debt and moral hazard. For decades, one of China’s primary engines of growth has been debt fueled construction. In the past few years, this engine of growth is running out of steam.

Since 2008, the amount of debt required to increase GDP output has been growing, but growth has slowed down. In the 11 years between 2008 – 2019, total debt from government, household, and businesses, increased from 169% of GDP to 306%, a 1.8x increase. Yet, for the same period, GDP growth rate slowed down, from 10% to 6% (Figure 2–left). Similarly, if you look at the total factor productivity (adjusted for expanding stock of buildings, machinery, and other capital), the rate has been negative since 2015 (Figure 2–right). Note: these are official numbers – which is likely on the optimistic side of things…

Notice that in Figure 2–left above, the fastest growing segment of debt is debt by non-financial companies. This is why Beijing is clamping down on Evergrande and real estate speculation.

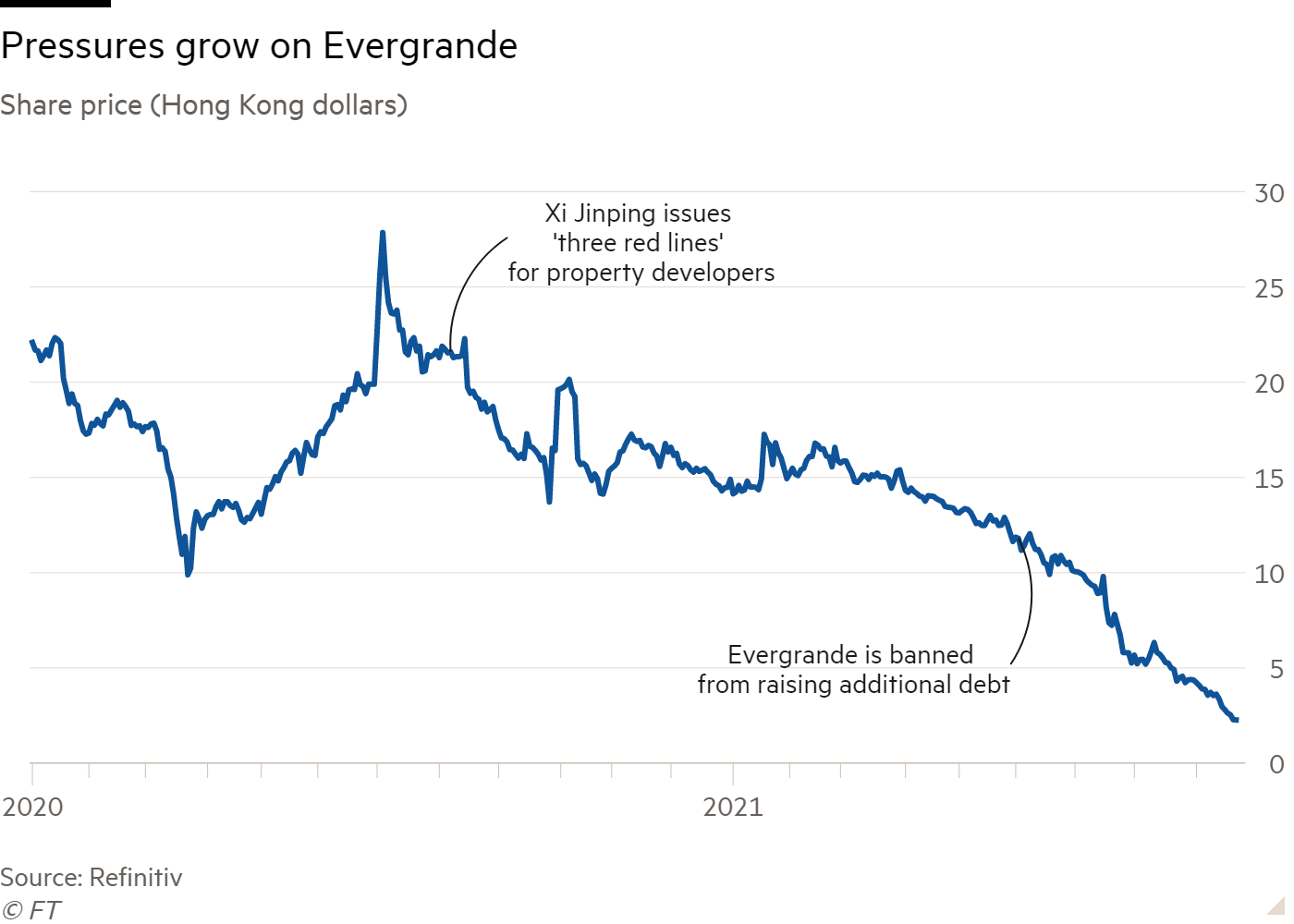

In 2017, President Xi Jinping said that “Houses are built to be inhabited, not for speculation”.

As it currently stands, the Chinese real estate sector is about 29% of GDP. This number is higher than the share of real estate in the US GDP pre-mortgage crisis of 2008, and higher than even the peak of the real estate bubble in 1980s Japan. The level of over-building in China is unprecedented. It is estimated that there are enough empty homes to house 90 million people. That’s enough to house the entire population of Germany, with room to spare.

To reign in the real estate sector, last year, regulators imposed the three red lines, which included hard limits on debt to asset/liquidity ratios that, if breached, will prohibit the company from raising more debt. Although the restriction is not specifically targeted on Evergrande, the company is the first and most prominent domino to fall. It was unable to meet the criteria imposed by regulators and earlier this year, was banned from raising more debt.

With more than $300 billion in liabilities (or about 2% of China’s GDP), Evergrande is the most indebted company in the world (mostly domestic debt though). It is also the largest real estate developer in China, employing more than 200,000 employees. As early as June 2021, regulators have asked major banks to perform stress tests on their Evergrande exposure, and just this month, Beijing has asked local governments to prepare for the company’s failure.

It’s unclear how this situation will play out. If Evergrande fails:

- The likely scenario is that the government will bail out retail investors and homeowners first. Local vendors and construction companies are likely second in line – this is important to prevent risk of contagion. And, last in the hierarchy are likely foreign creditors.

- The crisis will lead to a slow down in real estate transactions. As it is, home sales have started to slump. Potential homebuyers will continue to lose confidence in the developers’ ability to complete projects, making pre-selling unfinished homes even more difficult, further deepening the liquidity crisis in the real estate market.

- Commodity prices will be more volatile. The slow down in the construction sector caused steel demand to decline. As a result, the price of iron ore tumbled.

Nevertheless, if regulators stepped in to guarantee Evergrande’s debt, the problem with moral hazard will continue, making it very difficult for China to shift away from a debt fueled GDP growth model.

Why is Beijing doing all of this?

When viewed individually, it may appear that the clamp down appears to be sporadic. But when looked at as a whole, there appears to be a systematic approach. China appears to be entering a new phase of development.

“Communism with Chinese Characteristics” is a set of policies adopted by the CCP which is a version of Marxist Leninism that has been adapted to Chinese circumstances and that can be altered depending on the different time periods.

Introduced in the late 70s, the Deng Xiaoping theory (named after the famous architect of Chinese economic reform that led the opening up of the economy) states that the capitalist market economy is not contradictory to socialism. The theory stipulates that China needs to develop material wealth and economic growth before it can pursue a more egalitarian form of socialism. Or as more eloquently stated by the man himself: “let a few get rich first”. To achieve this, the market economy was a tool for development. And now that China is the second largest economy in the world, it is transitioning to a new era. Under Xi Jinping, the priority is shifting to “common prosperity for all”.

To achieve this goal, there are five strategies:

- High-quality development: means the ideal economic growth is one that is fueled by an increase in household income (not debt), export, and business investments (in strategic industries). This is why Beijing is clamping down on gambling and debt fueled real estate.

- Common prosperity: as the name suggests, means minimizing wealth gaps, even if it has to be engineered by the state via trickle-down economics. This is why Beijing is clamping down on the ultra wealthy and forcing them to contribute their wealth to reduce inequality.

- Building rule of law: means that the directive will come from the CPC. This is why Beijing is taking board seats in these leading companies.

- Domestic-international dual circulation: means that in addition to the export-led development model, China has to develop a robust domestic consumption economic model (again, hopefully, not debt fueled). Beijing still struggles with this. It’s hard to maintain credibility in the international market when the policies wipe out the wealth of public investors.

- Maintaining family values: is why Beijing forced ed-tech companies to be non-profits. The goal is to exert more control on educational content and to ensure that education cost is not prohibitive to the middle class (or at least that is the hope – some argue that without a more cost effective online solution, cost will increase instead). Note: this is also why China is limiting gaming for the young and banning effeminate men from TV.

Ok, so the goal is “common prosperity for allâ€, but why now? There’s one more data point worth considering: China is experiencing population decline.

China versus population decline

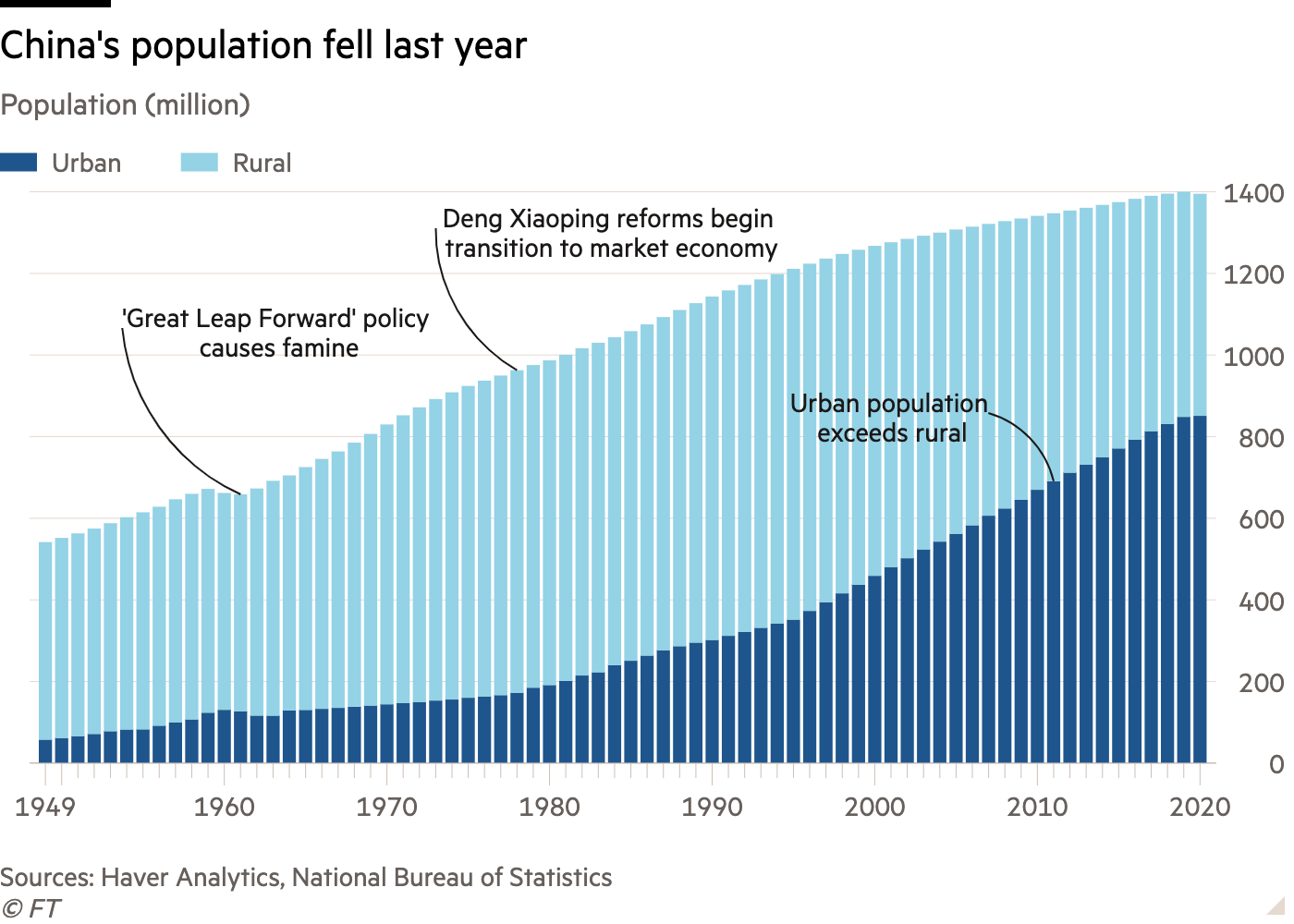

China is facing a demographic crisis at an unprecedented scale. Here is China’s population growth trend (Figure 4).

Here are some key takeaways from its latest census:

- In 2020, the population actually declined.

- In the 10 years between 2010 to 2020, China only added 72 million people (or ~5% growth).

- The estimate of the number of children born over a woman’s lifetime currently stands at only 1.3. This is far below the replacement rate of 2.1 (it takes two parents to produce a child).

- As a result, the population of the young will continue to shrink. The number of people in the working age group (between 15 to 50 year olds) has been shrinking since 2011, while the share of people older than 60 has gone up from 10.4% in 2000 to 17.7% in 2018.

- It is estimated that by 2050, one third of Chinese will be older than 60. This is a very bad trend because this means that (1) labor pool declines (which is bad for economic productivity and reduces tax sources), and (2) more elderly for the young to take care of (increases the pension burden for the state and also means a higher cost of healthcare).

- To make matters worse, there’s a significant gender imbalance between men and women. In 2019, there were 30 million more Chinese men than women (influenced by the one-child policy from the 80s, the cultural preference of having sons, and easy access to pre-natal scans). As a result, bride trafficking from South East Asia to China is becoming more prevalent.

It is unclear whether Beijing will succeed in reversing its population decline and carry out economic reform. What is clear from the outside, however, is that in the short term, the cost can be high. From the perspective of the investor, investing in China translates to a much higher risk premium.

You might be thinking, I can navigate these complexities – Having read 2,295 words of this article, I see the method to the madness – we should just invest in industries that Beijing wants to promote. Afterall, one of the tenets of socialism is that the worker owns the means of production. Before you jump in though, remember that what is strategic for Beijing is an area of concern for the US. Strategic industries have been sanctioned and pushed out of the US markets before.